1. Executive Summary

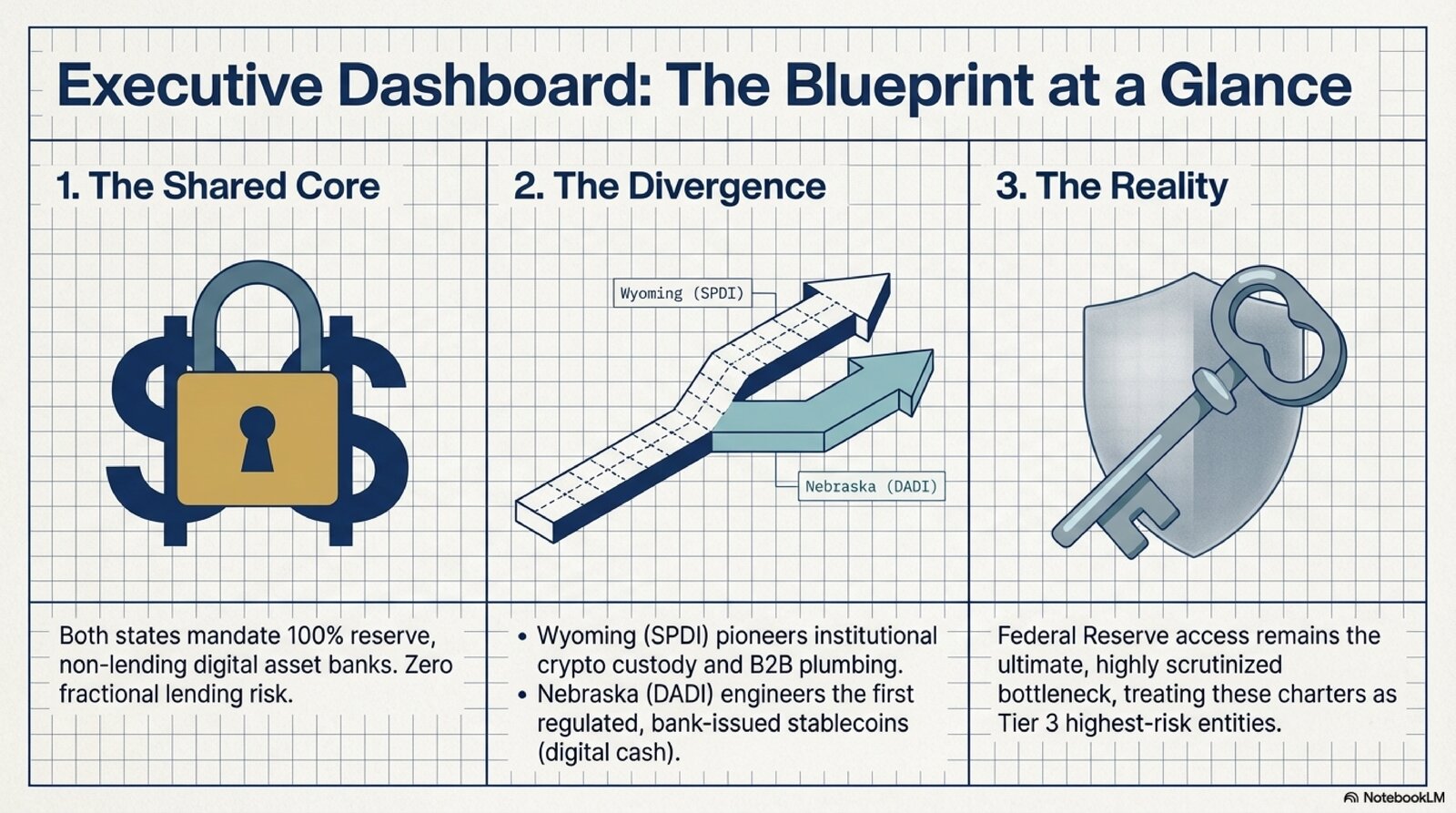

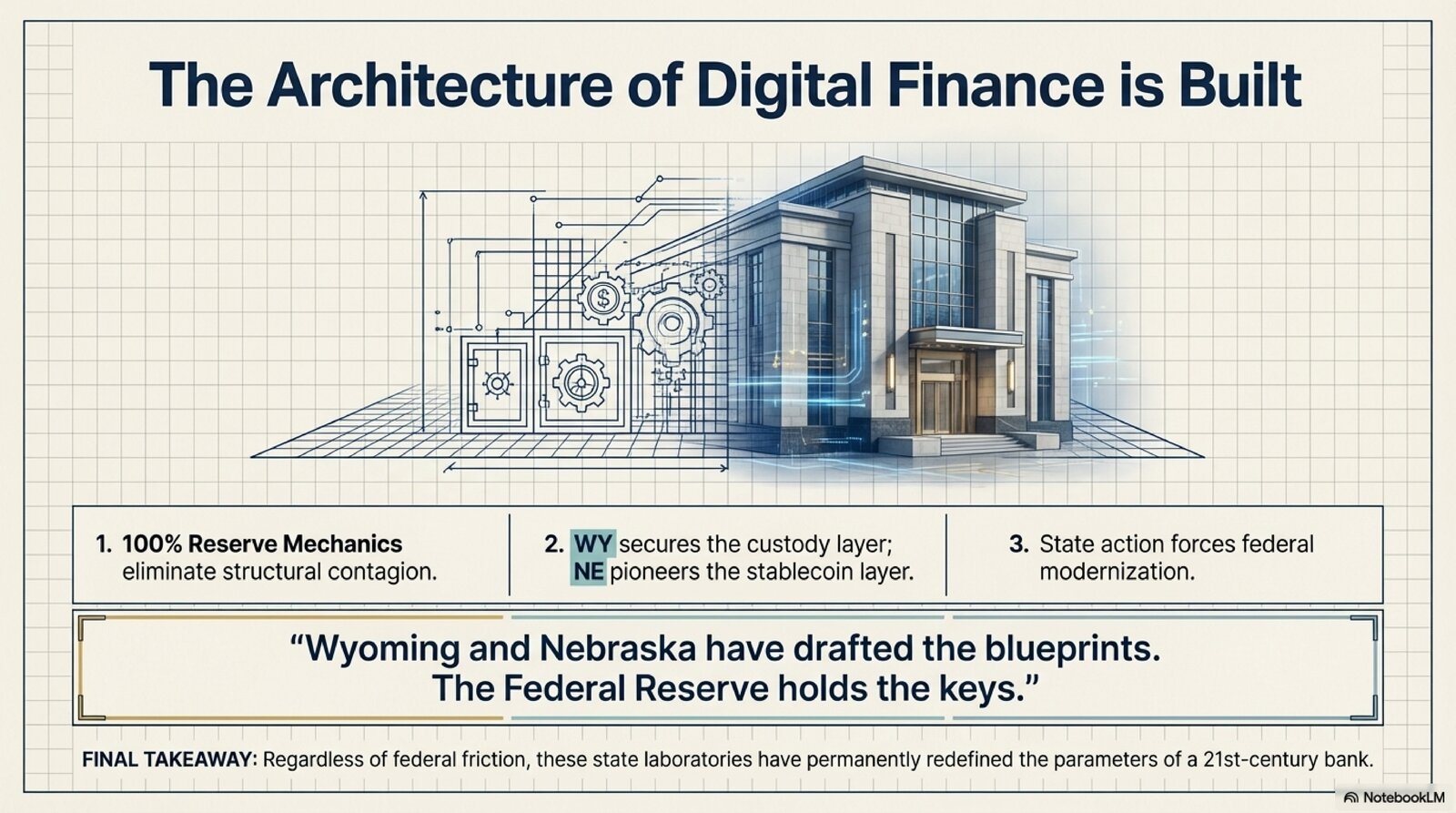

Wyoming and Nebraska have pioneered two distinct state bank charters to bridge digital assets with the traditional financial system. Wyoming’s Special Purpose Depository Institution (SPDI) charter, established in 2019, and Nebraska’s Digital Asset Depository Institution (DADI) framework under the 2021 Nebraska Financial Innovation Act (NFIA) both enable fully-reserved, crypto-focused banks that can custody digital assets and connect to U.S. dollar payment rails. Each model aims to foster fintech innovation while maintaining 100% reserve requirements (no fractional lending) for stability.[1][2] There are, however, important differences in scope and emphasis:

- Shared Approach: Both the SPDI and DADI charters create non-lending banks that hold fiat reserves equal to 100% of customer deposits.[1][2] These institutions cannot offer standard checking accounts or make conventional loans, focusing instead on custody, payment services, and other “banking-adjacent” digital asset services.[3][4] The goal is to provide crypto businesses a regulated home in the banking system without introducing traditional bank run risks.

- Key Difference – Stablecoins: Nebraska’s framework explicitly authorizes stablecoin issuance by its digital asset banks,[2] reflecting a focus on regulated digital USD tokens. The first Nebraska-chartered DADI (Telcoin Digital Asset Bank) can “mint” a U.S. dollar-backed stablecoin (e.g. eUSD) under state supervision.[5] Wyoming’s SPDI law does not mention stablecoins directly; SPDI banks primarily emphasize custody and fiduciary services. (Wyoming’s Custodia Bank did propose a proprietary “digital cash” token, Avit, but faced Federal Reserve resistance.[6][7]) In short, Nebraska positions itself as a pioneer in bank-issued stablecoins, whereas Wyoming initially led on crypto custody integration.

- Federal Reserve Access – Open but Uncertain: Both charters legally permit applying for Federal Reserve master accounts (direct payment system access).[4] This is a critical potential advantage, enabling crypto banks to clear payments directly through the Fed. In practice, however, Fed access has been limited. Wyoming SPDI banks encountered hurdles: the Fed denied Custodia’s request in 2023 over “safety and soundness” concerns with its crypto-heavy model. Only in March 2026 did the Fed cautiously grant Kraken’s SPDI a one-year pilot master account[8] – the first ever for a crypto-native bank. Nebraska’s law similarly invites Fed membership, but its lone DADI (Telcoin) has yet to obtain an account. Bottom line: the door to Fed access is open on paper, but in reality it remains subject to intense federal scrutiny and evolving guidelines.

In sum, Wyoming’s SPDI and Nebraska’s DADI offer two paths for integrating digital assets into U.S. banking. Both share a conservative, full-reserve foundation, but diverge in features like stablecoin services and regulatory approach. These state initiatives are shaping the national conversation on crypto banking, foreshadowing how federal policy might adapt. The following report provides an in-depth comparison – from legal structure and operational mandates to the experiences of the first chartered institutions – and examines what these developments mean for the future of fintech and banking policy in America.

2. Introduction and Background

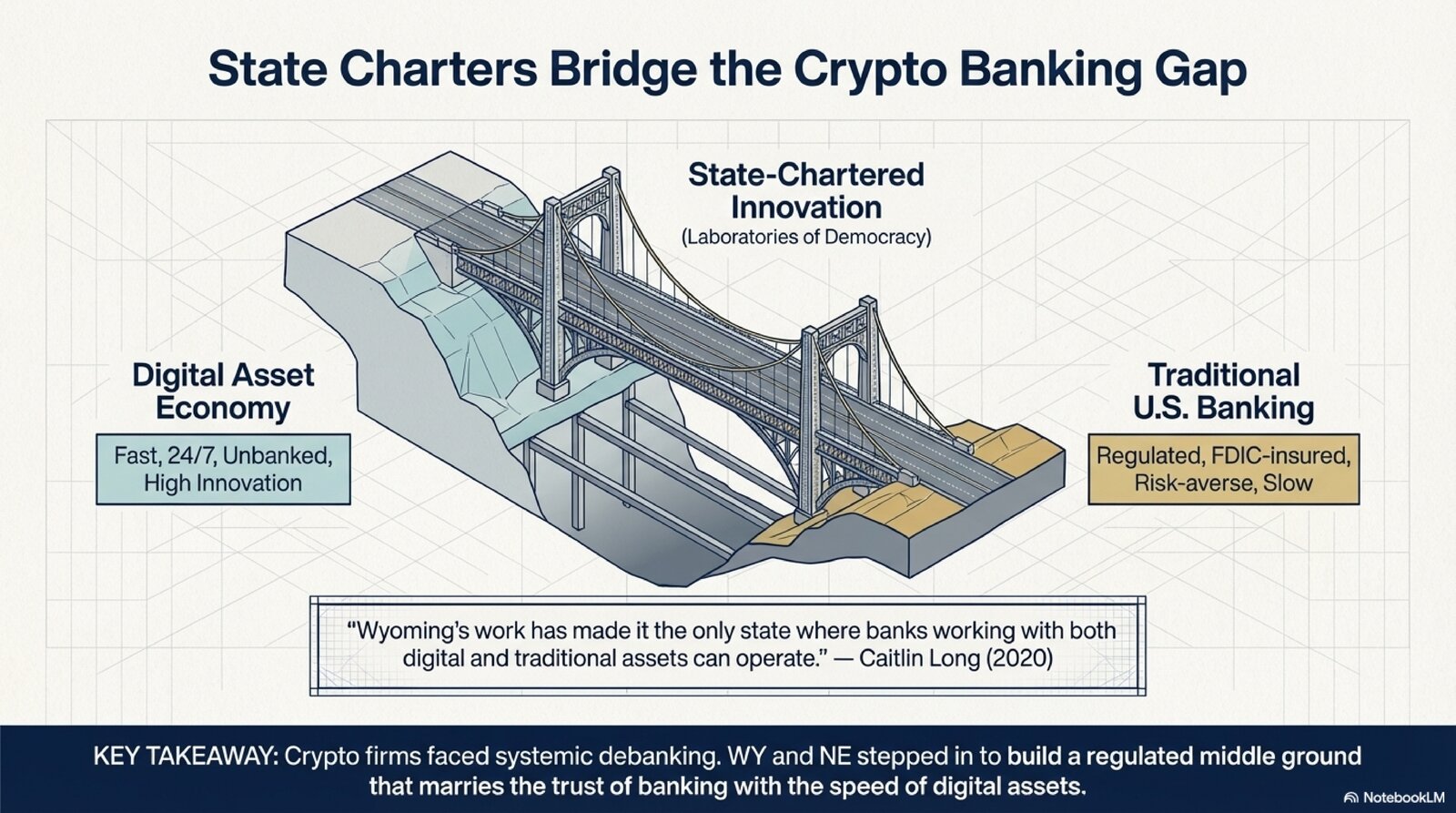

In the late 2010s, as the cryptocurrency industry expanded, crypto companies faced a pressing problem: lack of access to traditional banking. Many banks were unwilling or unable to serve digital asset businesses due to regulatory uncertainty and compliance risks. This “crypto banking gap” threatened to stifle innovation, as legitimate blockchain firms struggled to maintain basic accounts or payment services. In response, forward-thinking states began crafting new frameworks to marry the trust of banking with the innovation of crypto.

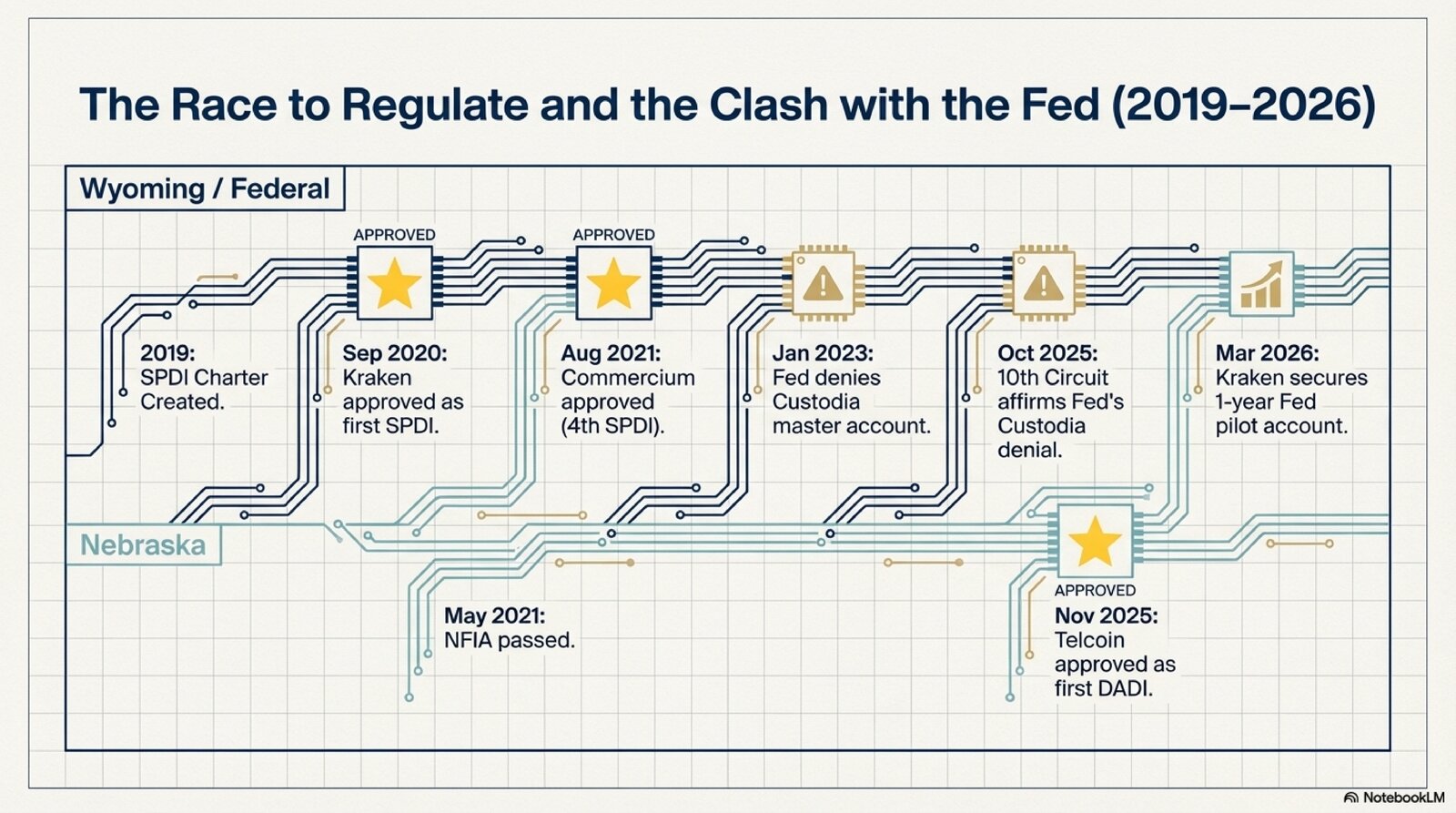

Wyoming emerged as an early leader. In 2019, it enacted legislation (House Bill 74) to create a novel bank charter called the Special Purpose Depository Institution (SPDI).[1] The SPDI was designed to be a “crypto bank”: a state-chartered depository institution that could handle digital assets and connect to the Federal Reserve system, while mitigating risk through a full-reserve, no-fractional-lending model.[1] This initiative was part of a broader package of blockchain-friendly laws championed by Wyoming policymakers and industry advocates like Caitlin Long. The vision was to make Wyoming an attractive domicile for crypto and fintech firms, solving their banking woes and boosting the state’s tech economy.

“Wyoming’s work has made it the only state where banks working with both digital and traditional assets can operate.” — Caitlin Long, 2020[4]

The SPDI charter was a bold experiment to integrate digital assets into a regulated environment, offering crypto companies a path to become fully regulated banks.

Nebraska took notice. In 2021, Nebraska passed the Nebraska Financial Innovation Act (NFIA),[5] becoming the second state (after Wyoming) to authorize digital asset depository institutions. This effort was spearheaded by then-State Senator (now U.S. Congressman) Mike Flood, who framed it as a chance to spur innovation and job growth in Nebraska’s financial sector.[9] The NFIA established a new bank charter for “Digital Asset Depository Institutions” (DADIs) – Nebraska’s answer to Wyoming’s SPDI. By enabling state-chartered crypto banks, Nebraska aimed to attract fintech startups, stablecoin issuers, and blockchain projects to set up shop in the Cornhusker State. A notable motivation was to support ventures like Telcoin, a local blockchain-based fintech (founded in 2017 in Norfolk, NE) that sought a bank charter to issue a USD-backed stablecoin and offer cutting-edge payment services.

“This is about more than cryptocurrency. It’s about the technology of money, payments, and banking – and financial innovation right here in Nebraska.” — Telcoin CEO Paul Neuner

By embracing digital asset banking, Nebraska’s leaders hoped to stem brain drain, attract high-tech investment, and put Nebraska on the map as a fintech-friendly state.

Despite their distinct origins, both Wyoming and Nebraska shared a common objective: reconcile the world of digital assets with the regulated banking system. Each state crafted legislation to carefully balance innovation with consumer protection and financial stability. Key principles included requiring full reserves for deposits (to prevent bank runs), strictly limiting risky activities like lending, and imposing strong compliance standards (e.g. Bank Secrecy Act/AML programs) to address concerns about illicit finance. They also both recognized that lasting success would require federal acceptance – hence provisions allowing their new banks to seek Federal Reserve access.

The following sections delve into how each framework is structured and operates, and how they differ. We’ll start with a brief timeline of key events to see how these charters have unfolded in practice.

3. Timeline of Key Events

4. Legal and Regulatory Frameworks

Wyoming’s SPDI Framework

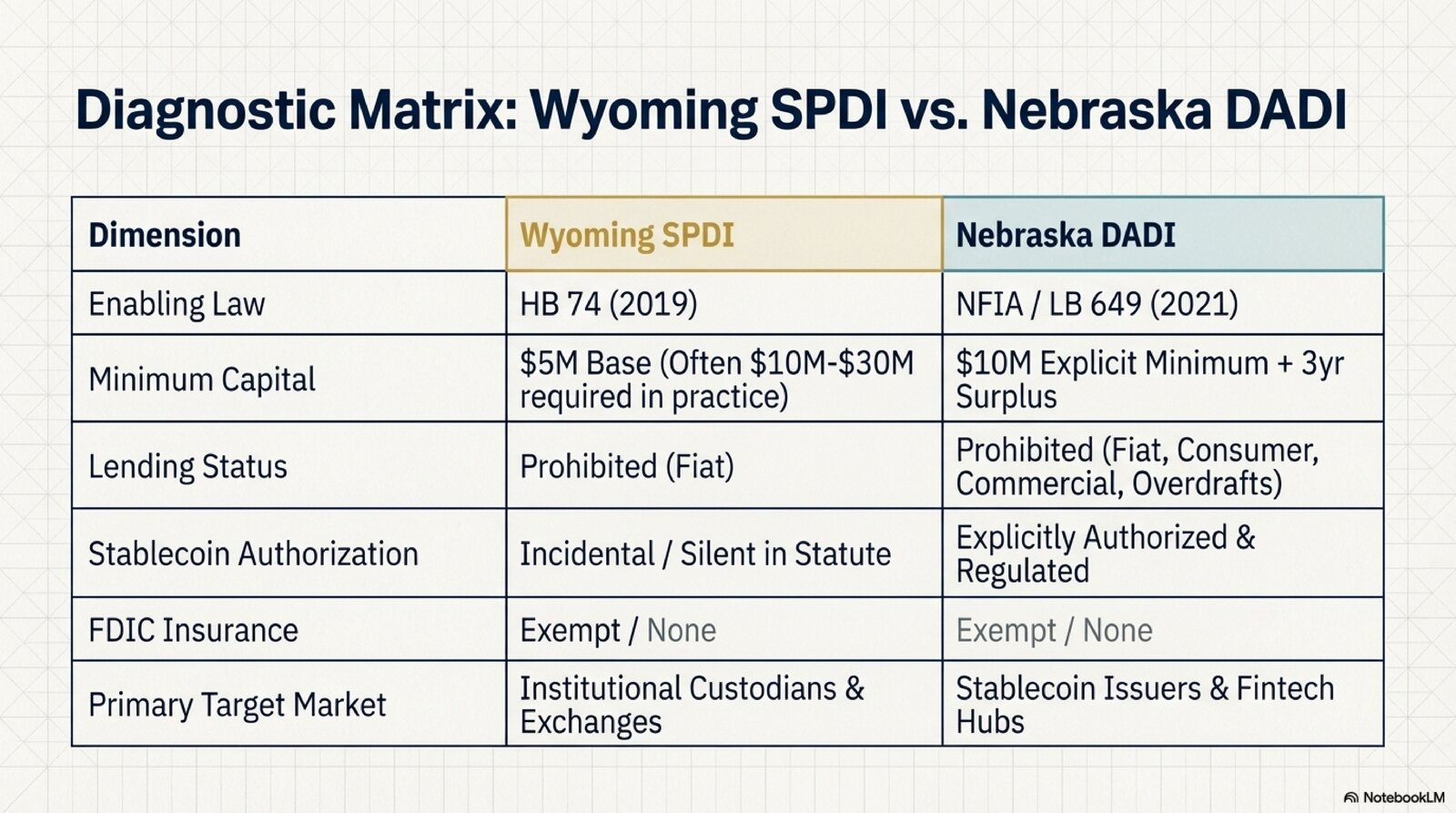

Wyoming’s SPDI charter was established by the Special Purpose Depository Institutions Act of 2019, now codified at Wyo. Stat. § 13-12-101 et seq. This law defines SPDIs as state-chartered banks with highly limited purposes: they may accept deposits and conduct incidental banking activities (like custody, fiduciary services, and payments) but must operate on a full-reserve basis and cannot lend against deposits. Wyoming simultaneously amended its Uniform Commercial Code (UCC) via SF 125 (2019) to provide a legal underpinning for digital asset custody and transactions. The Wyoming Division of Banking (within the Department of Audit) is the primary regulator, overseeing SPDI applications, examinations, and compliance. SPDIs are subject to most of Wyoming’s standard banking laws except where explicitly exempted (e.g. they are not required to obtain FDIC insurance). Over 2019–2021, Wyoming refined the framework with amendments (2020) and detailed regulations (2020/2021) to address technical aspects like liquid asset definitions, custody procedures, and capital guidance.

Crucially, Wyoming law anticipated federal interaction: SPDIs are eligible to apply for Federal Reserve accounts and services just like any state bank, though the statute doesn’t guarantee approval. The legislative intent was to position SPDIs as bridges between crypto finance and the Fed. By chartering SPDIs as State Member Banks (if they join the Federal Reserve System) or State Non-Member Banks (if not), Wyoming sought to integrate them into the federal banking ecosystem to the extent possible.

Nebraska’s DADI Framework

Nebraska’s Financial Innovation Act (LB 649), signed in May 2021, created Chapter 8, Article 30 of the Nebraska Revised Statutes – the legal basis for Digital Asset Depository Institutions. Nebraska’s law closely mirrors Wyoming’s concept but with a few notable differences and additional clarity on certain points (especially stablecoins). Under NFIA, a DADI can be chartered as a new Nebraska state bank dedicated to digital asset activities, or established as a digital asset depository division within an existing Nebraska bank. This two-track option lets traditional banks dip into crypto (by adding a department) or allows new entrants to form stand-alone digital asset banks.

Nebraska’s DADI is regulated by the Nebraska Department of Banking and Finance (NDBF), which oversees charter approvals, examinations, and rulemaking under NFIA. The Act mandated NDBF to draft implementing regulations (which Nebraska updated via LB 92 in 2023 to refine definitions and supervisory powers). The legislation is explicit about permissible activities and constraints: DADIs must follow all applicable state banking laws (on corporate governance, audits, etc.) except where specifically exempted. For example, NFIA exempts DADIs from Nebraska’s usual requirements to obtain FDIC insurance, since they won’t hold insured deposit accounts.

Both states’ laws reflect a careful balance between innovation and oversight:

- They require extensive vetting of charter applicants (background checks on owners and directors, detailed business plans, and public hearings). In Nebraska, a new DADI charter application must include a 3-year financial projection and evidence of at least $10 million in capital stock raised (refunded if the charter is denied). Wyoming’s statute initially required $5 million in capital and 3 years of expenses for an SPDI, though in practice the Banking Commissioner has discretion to demand more; guidance suggested $10–30 million might be needed depending on the business model.

- Both charters impose specialized supervision. Wyoming’s Division of Banking created an SPDI examination manual and “Capital Requirement Guidance” tailored to crypto asset risks. Nebraska’s NDBF likewise can set specific conditions on DADI operations and require additional safety measures (for example, bonding against operational risks, as NFIA details). Both regulators coordinate with federal agencies on BSA/AML compliance and (informally) on gauging how these institutions might fit into the broader banking system.

- The enabling laws also integrate consumer and systemic protections. Each DADI or SPDI must maintain robust cyber security, audit systems, and contingency plans. Wyoming originally required a “contingency account” (a special reserve for wind-down costs) for SPDIs, later tweaking this via amendments in 2020/2021. Nebraska’s law requires DADIs to keep a “community needs” file documenting how they serve the public and handle complaints, signaling an expectation of public accountability akin to Community Reinvestment Act principles.

In summary, Wyoming provided the template with a first-of-its-kind crypto bank charter, and Nebraska followed with a similar legal framework refined to its policy priorities (notably stablecoins and integration with existing banks). Both operate within the bounds of state banking law but push the envelope by authorizing activities (like digital asset custody and tokenization) that traditional banks have only cautiously approached.

🔑 Shared Vision: Full-Reserve Crypto Banks

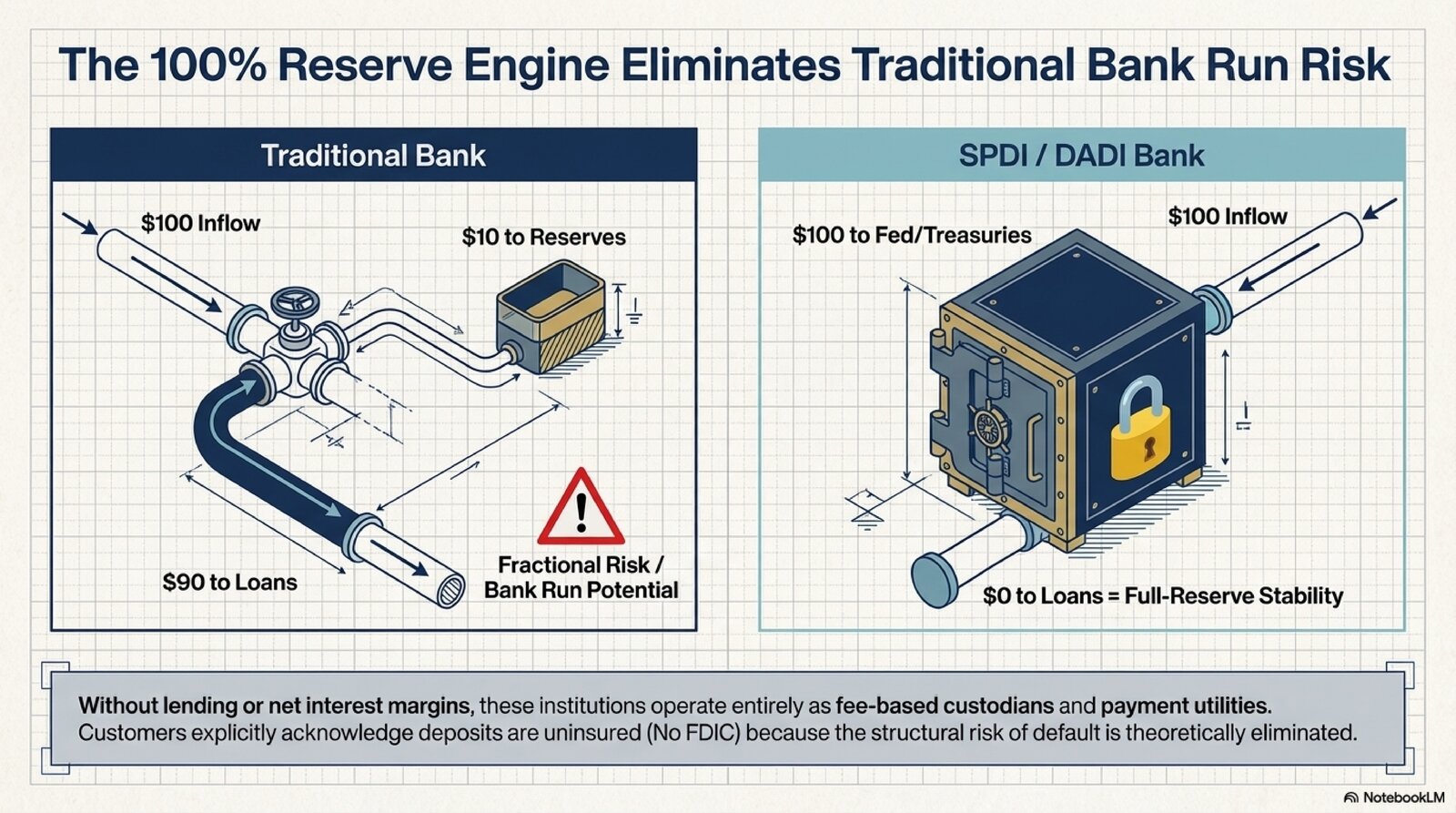

Both Wyoming’s SPDI and Nebraska’s DADI charters create 100% reserve banks focused on digital assets. Neither allows fractional-reserve banking – they can’t lend out customer deposits or run payment overdrafts. This ensures that if every customer demanded their money simultaneously, the bank could pay out in full. The trade-off is these banks operate more like custodians/payment utilities than traditional commercial lenders.

⭐ Emphasis on Stablecoins vs. Custody

Nebraska’s NFIA explicitly authorizes stablecoin issuance, aiming to let a state-chartered bank safely issue a USD-backed cryptocurrency. Telcoin’s eUSD is the first example. Wyoming’s SPDI law is silent on stablecoins, focusing instead on custody and fiduciary services. This underscores Nebraska’s intent to be a leader in regulated stablecoin banking, whereas Wyoming pioneered in crypto custody integration.

🔒 Federal Reserve Access: Permitted but Precarious

Both charters allow institutions to apply for Federal Reserve membership and accounts, envisioning direct access to Fed payment rails. However, approval is far from guaranteed. The Fed has treated these applications warily – grouping SPDI/DADI banks into its highest-risk review tier. Wyoming’s Custodia was denied Fed membership due to its “narrow” crypto focus and lack of FDIC insurance. Only in 2026 did the Fed grant Kraken a limited master account (effectively a pilot program). Nebraska’s Telcoin bank will likely face similar intensive scrutiny. In short, the legal path to Fed access exists, but federal regulators remain cautious, using case-by-case judgments to ensure any crypto bank connecting to the Fed meets stringent safety standards.

5. Charter Structures and Requirements

Corporate Structure and Formation

Both SPDI and DADI institutions must be incorporated as state-chartered corporations (not just LLCs or trusts). In Wyoming, an SPDI is chartered as a corporation through the State Banking Board and must include “SPDI” or similar in its name to signal its special status. Nebraska’s DADI law likewise requires a new bank to be formed under the Nebraska Model Business Corporation Act, or an existing Nebraska state bank to amend its charter to add a digital asset depository division. Nebraska mandates that a DADI’s main office and CEO’s primary office be located in Nebraska, anchoring management locally. Wyoming doesn’t statutorily require key personnel to reside in-state, but in practice SPDI applicants have maintained a significant presence in Cheyenne to satisfy regulators and demonstrate community benefit.

Capital and Surplus

Both frameworks impose substantial capital requirements upfront:

- Wyoming: The SPDI Act originally set a minimum capital stock of $5 million[10] to form the bank. Additionally, applicants had to demonstrate liquid assets to cover (initially) 3 years of operating expenses and establish a contingency fund equal to 2% of proposed deposits by year 3. However, Wyoming’s banking commissioner holds discretion to require more. In fact, guidance from 2020 indicated a prospective SPDI should plan for at least $10–30 million in capital depending on its business plan. For example, Kraken and Custodia each reportedly raised around $20 million of capital before launch, far above the base $5M, to satisfy supervisory expectations. Wyoming updated its law in 2021/2022 to streamline these capital rules (e.g. requiring 1 year of covered expenses instead of 3),[11] but the principle remains: SPDI capital must be “commensurate with risk,” often meaning a heftier buffer than traditional banks of comparable size.

- Nebraska: NFIA explicitly requires a minimum of $10 million in paid-in capital stock[2] for a newly chartered digital asset bank. Beyond that, the applicant must fund a surplus sufficient for at least 3 years of projected operating expenses (unless the regulator sets a different amount). This ensured, for instance, that Telcoin’s bank was well-capitalized to bear start-up costs – NDBF confirmed Telcoin met the $10M+ capital threshold and had ample surplus before granting the charter. Nebraska also limits ownership: bank holding companies can own DADIs, but subject to normal state/federal bank holding company regulations. As with Wyoming, Nebraska regulators can impose higher capital or liquidity requirements case-by-case to address particular risk profiles.

Regulatory Oversight and Exams

Once chartered, these institutions are supervised like banks, with some extra eyes:

- Wyoming Division of Banking supervises SPDIs through regular safety-and-soundness examinations, similar to those for state commercial banks. However, exam procedures have been tailored – Wyoming developed a SPDI Examination Manual and special guidance for digital asset custody, given the novel risks of private key management, cybersecurity, and volatility. SPDI banks must submit quarterly Call Reports to the state (the Division publishes these reports, providing transparency into their financial condition). Importantly, if an SPDI joins the Federal Reserve System, the Fed would also have exam authority. The Fed has already conducted pre-membership exams on applicants like Custodia, flagging weaknesses. Additionally, the Wyoming Banking Board retains oversight for major decisions, such as certificate of authority to commence operations and any revocation proceedings.

- Nebraska Department of Banking and Finance (NDBF) similarly examines DADIs on a routine schedule. NFIA stipulates that DADIs are subject to Nebraska’s bank exam statutes: examiners can review books, ensure compliance with all laws, and evaluate management’s fitness and risk controls. Nebraska included specific reporting requirements – DADIs must file periodic reports on their condition, to be made public, and face fines ($5,000 per day) for late reports. This transparency is meant to boost confidence. NDBF can also issue rules or orders to enforce safe operations and has power to suspend or revoke a charter for violations or unsafe practices. Both states additionally require coverages like surety bonds and insurance against operational risks (e.g. cyber breaches, officer errors), recognizing that crypto platforms are targets for hacking and technical failures.

Deposit and Lending Restrictions

These define the “special purpose” nature of SPDI/DADI banks and set them apart from normal banks:

- No Demand Deposits: Neither SPDI nor DADI can accept traditional checking accounts or other demand deposits withdrawable by third-party payment methods. Wyoming’s law explicitly forbids SPDIs from offering deposit accounts that can be drawn by check or draft, except for certain fiduciary accounts. Nebraska’s law copies this: “A digital asset depository institution shall not accept demand deposits of U.S. currency or deposits that may be withdrawn by check or similar means for payment to third parties.” In practice, this means these banks don’t hold your everyday checking account – they hold digital asset accounts and custody balances, and any fiat they receive is for the purpose of conversion or custody, not general spending.

- No Fiat Lending: Both frameworks prohibit making loans or extending credit in fiat currency. Wyoming SPDIs cannot loan out any customer deposit dollars. Nebraska DADIs are similarly barred from lending in USD – the statute goes further to ban consumer loans, commercial loans, mortgages, and even overdraft credit lines. The Nebraskan DADI can, however, “facilitate” digital asset lending or borrowing between customers or via DeFi platforms as a service (e.g., help customers stake assets or post crypto as collateral for loans from others). But the DADI itself can’t be the lender of record for fiat. Essentially, the business model is fees for services, not interest from loans.

- 100% Reserve Requirement: This is a cornerstone of both charters. At all times, an SPDI/DADI must hold liquid assets at least equal to 100% of its deposit liabilities – in other words, every dollar (or crypto) deposited is backed by a dollar in reserve. Liquid assets are defined to include cash on hand, balances at Federal Reserve Banks or FDIC banks, U.S. Treasuries, and in Wyoming even certain highly-rated corporate or municipal bonds within limits. Nebraska’s NFIA similarly requires DADIs to maintain “at all times, liquid assets equal to 100% of the value of digital asset deposits.” Under NFIA, any U.S. currency received from customers must be placed in an FDIC-insured institution in Nebraska (or invested in approved safe assets like short-term Treasuries). The full-reserve rule is why these charters are often dubbed “narrow banks” or “full-reserve banks.” It also explains why FDIC deposit insurance isn’t required: since the bank isn’t loaning out deposits, the risk of default is theoretically low, and if the bank fails, all customer funds should still be there (in a segregated form). Indeed, customers must acknowledge that their deposits aren’t FDIC-insured.

- Other Limitations: SPDI and DADI banks can engage only in activities permitted by their charter and approved in their business plan. They cannot operate completely like a normal retail bank. Both types of institutions must also use specialized terminology in branding: Wyoming requires “SPDI” or similar in the name; Nebraska requires a newly chartered DADI to use “digital asset bank” in its name to avoid confusion with regular banks. This is a consumer protection measure to make clear the difference in services.

Customer Eligibility and Protections

The new charters impose criteria to ensure these banks deal with informed, legitimate customers:

- Customer Due Diligence: NFIA mandates that DADIs only do business with customers who provide evidence of compliance with anti-money-laundering (AML) laws and, if entities, proof of lawful operations. Essentially, a DADI must perform rigorous KYC (Know Your Customer) and ensure that, say, a corporate client is a real operating company not engaged in illicit business. Wyoming’s approach with SPDIs was to target professional and institutional clients by default. In practice, Kraken’s SPDI will serve retail customers but must implement strong KYC/AML programs equivalent to any bank (both states require BSA/AML compliance programs meeting federal standards).

- Disclosure of Risks: Both states require that customers be clearly informed about the nature of the bank and its products. For example, NFIA Section 8-3008 lists numerous mandated disclosures to every DADI customer: including a statement that digital asset deposits are not FDIC-insured and that digital assets are volatile and may result in loss. Also, any advertising or website must conspicuously note the lack of FDIC insurance and the speculative risk involved in crypto holdings. Wyoming’s SPDI rules similarly require clear notice that deposits are uninsured and that the institution is a special purpose bank.

- Community Obligations: An interesting aspect of Nebraska’s law is a quasi-“Community Reinvestment” requirement for DADIs to help meet local digital financial needs. A DADI must maintain a public file describing how it’s supporting the community (e.g., through digital finance education or services). This is unusual for a non-lending institution, but it reflects a legislative intent that even a cutting-edge digital bank should benefit Nebraskans broadly, not just serve remote crypto traders. Wyoming’s SPDI law did not have an analogous provision, as SPDIs were envisioned more as B2B institutions initially.

The strictures above delineate these charters as narrowly focused banks with a fintech twist. By removing lending and limiting deposits, they eliminate classic bank failure modes at the cost of giving up traditional revenue streams (like loan interest). As we’ll see in later sections, this heavily influences their business models.

6. Operational Models and Restrictions

This section describes what these banks can and cannot do on a day-to-day operational level, with a focus on custody, reserve management, and how they serve customer needs within their legal constraints.

Custody of Digital Assets

Providing secure custody for cryptocurrencies and other digital assets is a core function of both SPDI and DADI banks. In essence, these institutions serve as regulated custodians where customers can deposit their bitcoins, ether, tokens, or private keys for safekeeping, much like one would deposit cash in a bank vault. Both Wyoming and Nebraska adjusted their laws to accommodate this:

- Wyoming enacted its digital asset law (W.S. 34-29-104) clarifying that digital assets can be property under custody of a bank and setting forth a regime for perfection of security interests in crypto. This gave SPDIs (and Wyoming trust companies) legal certainty to hold crypto on behalf of clients, whether as custodian or fiduciary.

- Nebraska’s NFIA doesn’t explicitly rewrite property law (beyond incorporating the uniform term “controllable electronic record” for digital assets), but in practice it authorizes DADIs to hold digital assets in custody and even act as “qualified custodians” for investment advisers under SEC rules. NFIA and its regulations ensure any crypto custody is backed by appropriate controls: multi-factor authentication, cold storage solutions, insurance against theft, etc., as overseen by NDBF.

Operationally, a DADI or SPDI custody arrangement likely means the bank holds the private cryptographic keys to the customer’s digital wallets in a secure environment (often using hardware security modules or multi-signature schemes). The bank would maintain detailed records mapping each digital asset to each customer, and crucially, those assets remain off the bank’s balance sheet (they are customer property, not the bank’s own investment, except for the fiat reserves corresponding to stablecoin or deposit balances). This segregation is important: if the bank were to fail, by law the customer’s digital assets are not available to general creditors – they should be returned to customers after paying custodial fees or costs.

For customers, using an SPDI/DADI for custody offers regulatory protections: the bank has bonding, cyber insurance, regulatory exams, and legal obligations as a custodian. It’s a middle ground between entrusting assets to an unregulated exchange (which could fold or be hacked, as seen in numerous crypto exchange failures) and self-custody (which is technically challenging and risky for many). These state banks aim to be a sort of “crypto safety deposit box” – secure and supervised.

Payments and On/Off-Ramps

Both charters allow the banks to facilitate payments in both digital assets and fiat:

- Fiat Payments: While they can’t offer traditional checking accounts, they can still enable clients to transfer money. For example, an SPDI can provide wire transfer services, ACH transfers, or debit card-like functionality so long as it’s drawing on 100%-reserved funds. Kraken’s SPDI, for instance, planned to issue Visa debit cards linked to fiat deposit balances held at Kraken Bank – when a customer spends, Kraken Bank would simply move the equivalent funds (which were fully reserved) to the merchant’s bank via standard payment networks. DADIs in Nebraska can similarly “provide payment services upon the request of a customer” – meaning they can connect to payment systems to let customers send or receive funds. The difference is the money must always be there to back any payment.

- Digital Asset Transfers: SPDI and DADI banks can also transfer crypto on behalf of customers – e.g., sending Bitcoin from the bank’s custody wallet to another wallet per client instructions. This is part of being a custodian with “authorized transactions on behalf of customers.” Wyoming regulations cover how a bank must validate authenticity of customer orders, secure consensus on blockchain transactions, and handle forked coins or airdrops. Essentially, these banks can act as a crypto transaction processor: instead of the customer fiddling with private keys, the bank does it for them under strict protocols.

A major operational boon would be if these banks have direct Federal Reserve accounts – that would allow near-instant settlement of fiat payments internally and with other banks, improving efficiency. Without a Fed account, SPDIs/DADIs must partner with correspondent banks for Fedwire/ACH access, adding dependency on traditional banks.

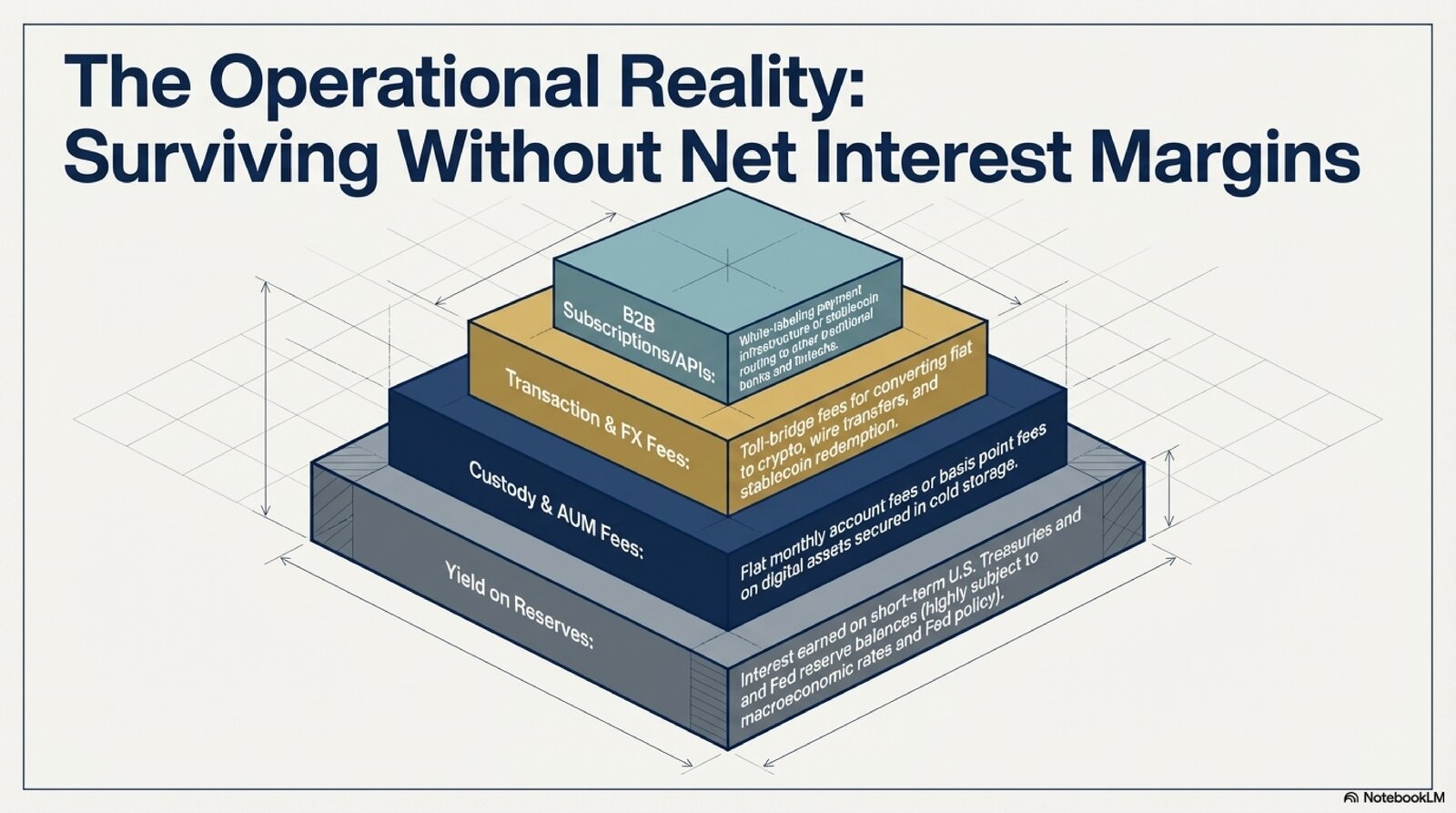

Revenue Model Constraints

Because they can’t lend or invest deposits to earn interest, how do these banks make money? They must rely on fee-based and off-balance-sheet activities:

- Custody Fees: Charging clients for holding digital assets securely (much like a custody or asset management fee). This could be calculated as a basis point fee on assets under custody or a flat monthly account fee.

- Transaction Fees: If the bank facilitates trades or transfers – for instance, moving crypto between exchanges or converting crypto to fiat – it can collect service fees. Kraken Bank, integrated with Kraken Exchange, could earn fees by streamlining the trading settlement process for Kraken’s customers.

- Payment Services Fees: Fees for wire transfers, stablecoin issuance/redemption fees, API access fees for fintech integration, etc.

- Ancillary Services: Some SPDIs may offer consulting on blockchain enterprise solutions, compliance services for crypto (like help with tax lot reporting for held assets), or even white-label their stablecoin or payment infrastructure to other banks for a fee. Telcoin’s model, for example, involves partnering with telecom providers and other banks to extend stablecoin remittance services, which could generate transaction fees or revenue-sharing.

The prohibition on lending means they won’t earn net interest margin (NIM) like a normal bank, and the full reserve requirement means they can’t invest heavily in long-term securities either – they need liquidity. They may hold some Treasuries for reserves, and that interest income helps offset costs, but regulatory expectations likely keep durations short.

Compliance Operations

Both categories of bank must run heavy-duty compliance departments:

- BSA/AML: They are on the hook for policing against money laundering and fraud. Every customer and transaction must be screened. With crypto involved, that means robust blockchain analytics – e.g., monitoring for coins coming from illicit addresses or mixers, using blockchain forensics tools to ensure they aren’t aiding unlawful activity. They also have to file Suspicious Activity Reports (SARs) and Currency Transaction Reports (CTRs) like any bank.

- Cybersecurity: Given the digital-native nature, regulators expect top-tier information security. Multi-layered defense, regular penetration testing, cryptographic key management ceremonies – all these become routine. A single security breach could be fatal to confidence (and to the charter).

- Audit and Transparency: These banks likely undergo both state regulatory audits and independent financial audits. They might even publish proof-of-reserves or other transparency reports to bolster trust (especially in the wake of high-profile crypto failures, demonstrating reserves are intact is valuable). In Telcoin’s case, being the first regulated stablecoin bank, they have every incentive to show strong audits of their eUSD reserve backing.

In summary, the operational paradigm is one of high-trust, low-risk financial services. These banks promise not to gamble with your money – they won’t lend it out or leverage it. But in return, they charge explicit fees for services. It’s a throwback to old safe deposit box and account maintenance fee models, modernized for crypto. They aim to combine the tech agility of fintech (24/7 blockchain networks, rapid innovation) with the assurances of banking (regulation, audits, solvency). In practice, finding profitability in this model is uncharted territory – much depends on scale and possibly on offering higher-value services like stablecoin issuance or providing infrastructure to other fintechs.

7. Stablecoin Issuance and Custody Provisions

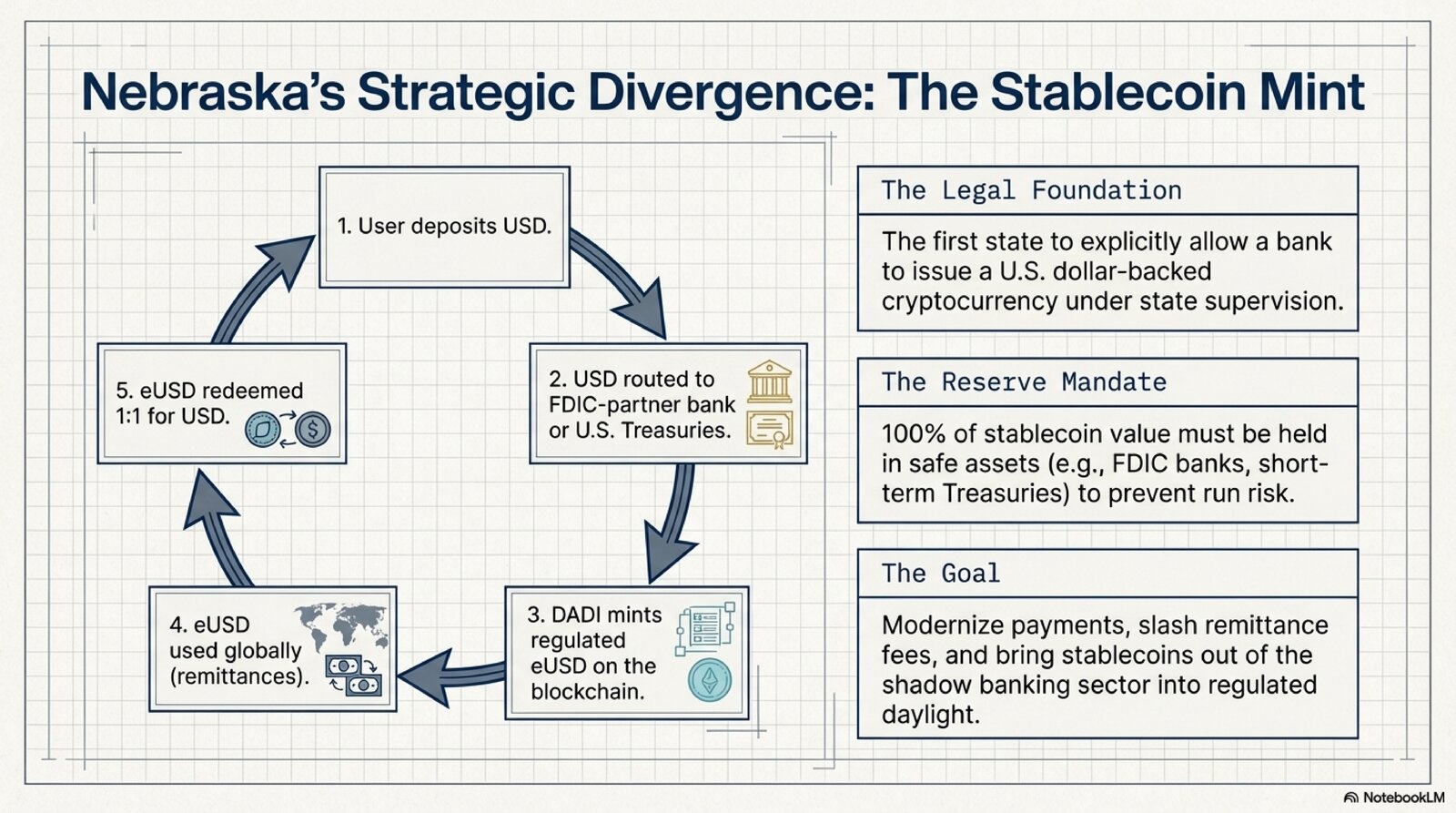

One of the most groundbreaking aspects of Nebraska’s NFIA is that it explicitly empowers a digital asset bank to issue stablecoins – making Nebraska the first state to allow a bank-issued cryptocurrency under state law. Stablecoins are digital tokens pegged to a stable asset (usually the U.S. dollar) and are integral to the crypto economy for providing dollar-equivalent liquidity. However, unregulated stablecoins (like Tether’s USDT) have raised concerns about reserve transparency and systemic risk. Nebraska’s approach essentially creates a class of regulated stablecoin issuers under banking supervision, potentially addressing those concerns.

Nebraska’s Stablecoin Framework

NFIA doesn’t go into deep technical detail, but it defines “stablecoin” as[2] “a controllable electronic record designed to have a stable value that is backed by a reserve asset.” This broad definition covers dollar-backed crypto tokens. Under NFIA:

- A DADI bank may issue stablecoins, provided it holds reserves equal to 100% of the stablecoin outstanding. The law specifically requires that stablecoin reserves be in the form of safe assets, like U.S. dollars on deposit in an FDIC-insured Nebraska bank or equivalent high-quality assets. For instance, Telcoin Digital Asset Bank’s eUSD stablecoin is backed by a pool of U.S. dollar deposits and short-term U.S. Treasury bills held at insured Nebraska institutions.[5]

- The bank effectively treats stablecoin issuance as a liability – when eUSD tokens are issued, Telcoin Bank creates a matching liability on its balance sheet (“Stablecoin tokens outstanding”) and holds an equal amount in reserve assets (cash/Treasuries) as an asset. This mirrors a money market fund or a currency board system, where every token is a claim on a real dollar in the bank.

- NFIA and NDBF oversight ensure that stablecoin issuance is done prudently: the bank must redeem tokens at par on demand (each eUSD should be redeemable 1-for-1 for $1), and marketing material must clarify that while eUSD is meant to be stable, it’s not FDIC insured and relies on the bank’s full reserve backing.

- Nebraska got here in part because Telcoin actively advocated for the law to enable its business model: to issue a blockchain-based remittance token for U.S. dollars. Telcoin’s success in obtaining a charter demonstrates the law’s intent.

Governor Pillen hailed the charter as allowing Nebraska to lead “a new era of digital payments” by enabling a bank that can mint stablecoins. NDBF Director Lammers likewise emphasized that the structure ensures “the payment is always good” – meaning each stablecoin is reliably backed by dollars/bonds.

The implications are significant: a Nebraska digital asset bank can now do what historically only central banks do – issue a form of digital money – but with each unit fully collateralized by central bank money (cash or equivalents). This transforms stablecoins from potentially murky “IOUs” issued by private startups into something more akin to electronic travelers’ checks issued by a supervised bank.

Wyoming’s Take

Wyoming’s SPDI law did not explicitly enumerate stablecoin issuance among allowed activities. However, the law’s broad phrasing (SPDIs can conduct “other activity incidental to the business of banking” and handle digital assets generally) left the door open. In practice:

- Custodia (Avanti) proposed the Avit: a programmable electronic USD instrument described as a digital negotiable instrument – essentially a stablecoin by another name. Avit was meant to serve institutional transactions without being a blockchain token that regulators would label a “deposit.” Custodia sought Fed approval for Avit, but the Fed’s denial order expressly noted Custodia’s plan to issue a crypto-asset token and viewed it as part of the novel and risky aspects of Custodia’s business model.[12]

- Other SPDIs like Kraken have not publicly discussed plans to issue their own stablecoin. Kraken might not need to, since it can integrate stablecoins like USDC on its exchange without the bank issuing them. But theoretically, a Wyoming SPDI could issue tokens.

- If we interpret Wyoming law, an SPDI issuing a stablecoin that’s fully reserved by dollars in its Fed account (should it have one) might be considered an incidental banking activity. However, because stablecoins weren’t explicitly in the statute, any SPDI doing so would likely require specific blessings from the Wyoming Division of Banking and careful coordination with the Fed.

Custody of Stablecoins and Digital Securities

Beyond issuing stablecoins, these banks can also custody stablecoins and tokenized assets issued by others. For example, a customer might deposit USD Coin (USDC) or Tether (USDT) with a SPDI/DADI for safekeeping. Or a company could use a SPDI to custody tokenized securities or NFTs. Wyoming’s statutes (via UCC amendments) made it possible for a bank to perfect security interest in digital securities, which could be big for digital asset markets.

Risk Management for Stablecoins

If a DADI or SPDI issues a stablecoin, it must manage a different set of risks:

- Run risk: If users lose confidence (even irrationally) and rush to redeem tokens, the bank must honor redemptions 1-for-1. With full reserves, this should be feasible, but if reserves are in bonds, fluctuations could threaten full value on short notice in stress scenarios. To mitigate this, a prudent stablecoin-issuing bank would keep the bulk of reserves in very short-term instruments (cash, overnight Fed balances, very short Treasuries) to minimize interest rate risk.

- Cyber/Operational risk: The bank has to ensure the smart contracts issuing the stablecoin are secure and that it can always control minting and redemption. Also, an operational failure (like losing keys or a blockchain outage) could disrupt redemption.

- Regulatory risk: If federal laws change (e.g., if Congress passes a stablecoin law requiring federal bank charters for issuers), a state-chartered issuer might have to adjust or seek a federal charter. Nebraska’s move essentially anticipates federal action and tries to fit within the likely framework.

Telcoin’s eUSD will be an interesting test case. It’s the first stablecoin issued by a depository institution in the U.S. under direct banking supervision. If it succeeds and gains adoption (even if just for remittances and telecom payments initially), it could demonstrate a blueprint for “stablecoin banks.” On the other hand, if it struggles to gain traction or faces unforeseen issues, that will be instructive too.

Other Digital Asset Business

Both charters allow some additional crypto-related operations:

- They can facilitate staking (putting crypto to work in proof-of-stake networks for rewards) and lending (peer-to-peer) as an intermediary. A bank might run nodes for networks or help customers stake assets while keeping custodial control (and taking a fee).

- They can serve as a platform for digital asset exchanges – maybe not an exchange themselves, but providing custody and banking for exchanges. For example, a SPDI can be the settlement bank for a crypto exchange, holding the exchange’s fiat and crypto reserves (Kraken’s SPDI basically does this in-house for Kraken’s exchange).

- They can hold stablecoin reserves for others. Possibly, a Nebraska DADI (besides Telcoin) could offer reserve holding services to third-party stablecoin issuers.

In conclusion, Nebraska’s DADI explicitly merges stablecoin innovation into the banking sphere, whereas Wyoming’s SPDI implicitly allows it but has been functionally more focused on custody. This difference underscores each state’s strategic focus: Nebraska aligned with a vision of modernizing payments with bank-issued digital cash; Wyoming concentrated on integrating crypto businesses into the existing financial system (providing the pipes and custody, but not necessarily reinventing money itself).

8. Federal Reserve Access

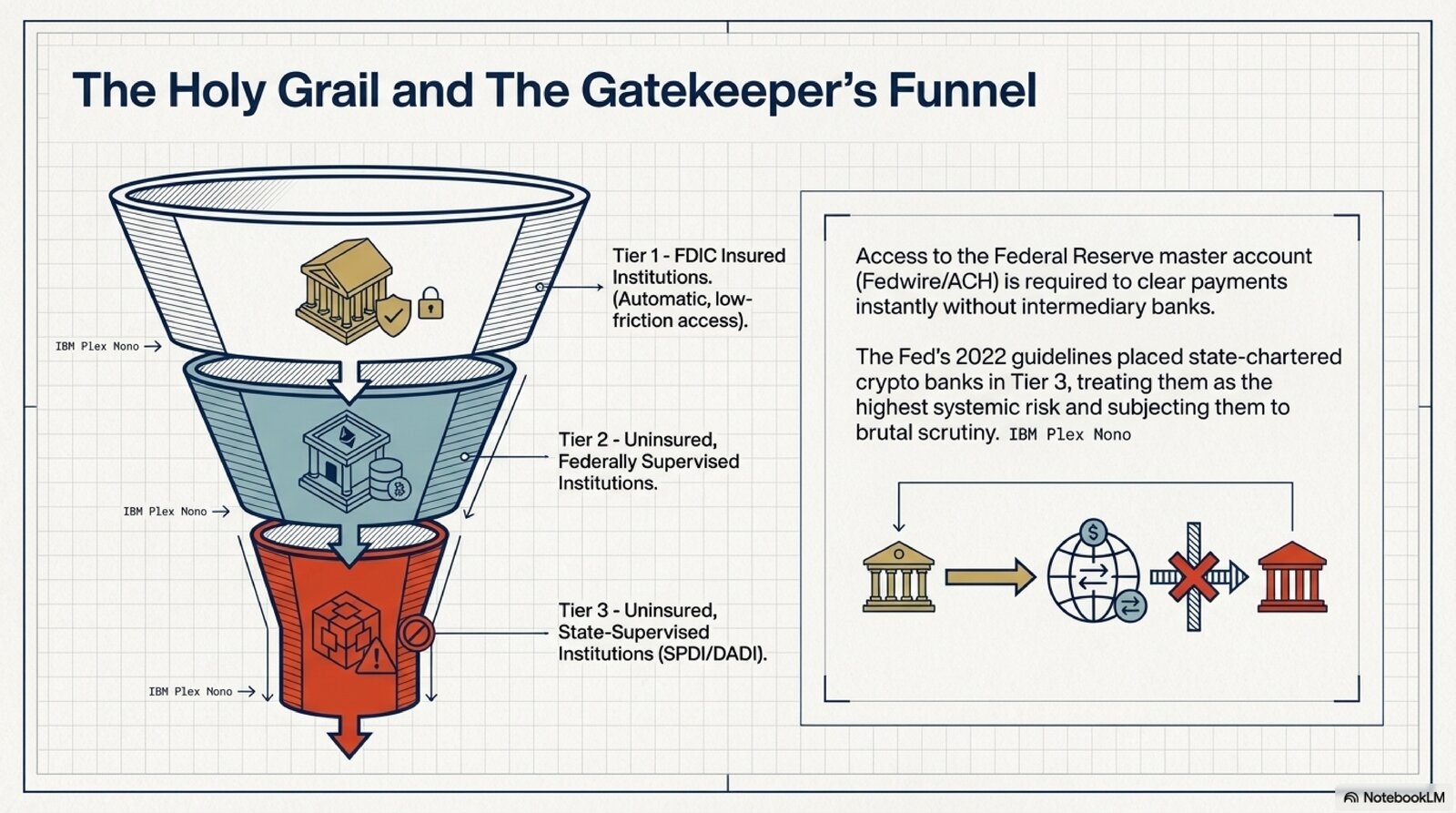

Access to the Federal Reserve – specifically, obtaining a Federal Reserve master account and, in some cases, Federal Reserve System membership – has been the make-or-break factor for the viability of these crypto bank charters. A master account allows a bank to directly use Fed payment services (Fedwire, ACH, etc.) and to deposit funds at the Fed. Traditionally, all federally insured banks get one by right, but for novel state-chartered institutions like SPDIs and DADIs, the Federal Reserve has considerable discretion. Both Wyoming and Nebraska explicitly contemplated Fed access for their chartered institutions, but the Federal Reserve’s cautious approach has led to a complex saga.

Wyoming SPDI and the Fed

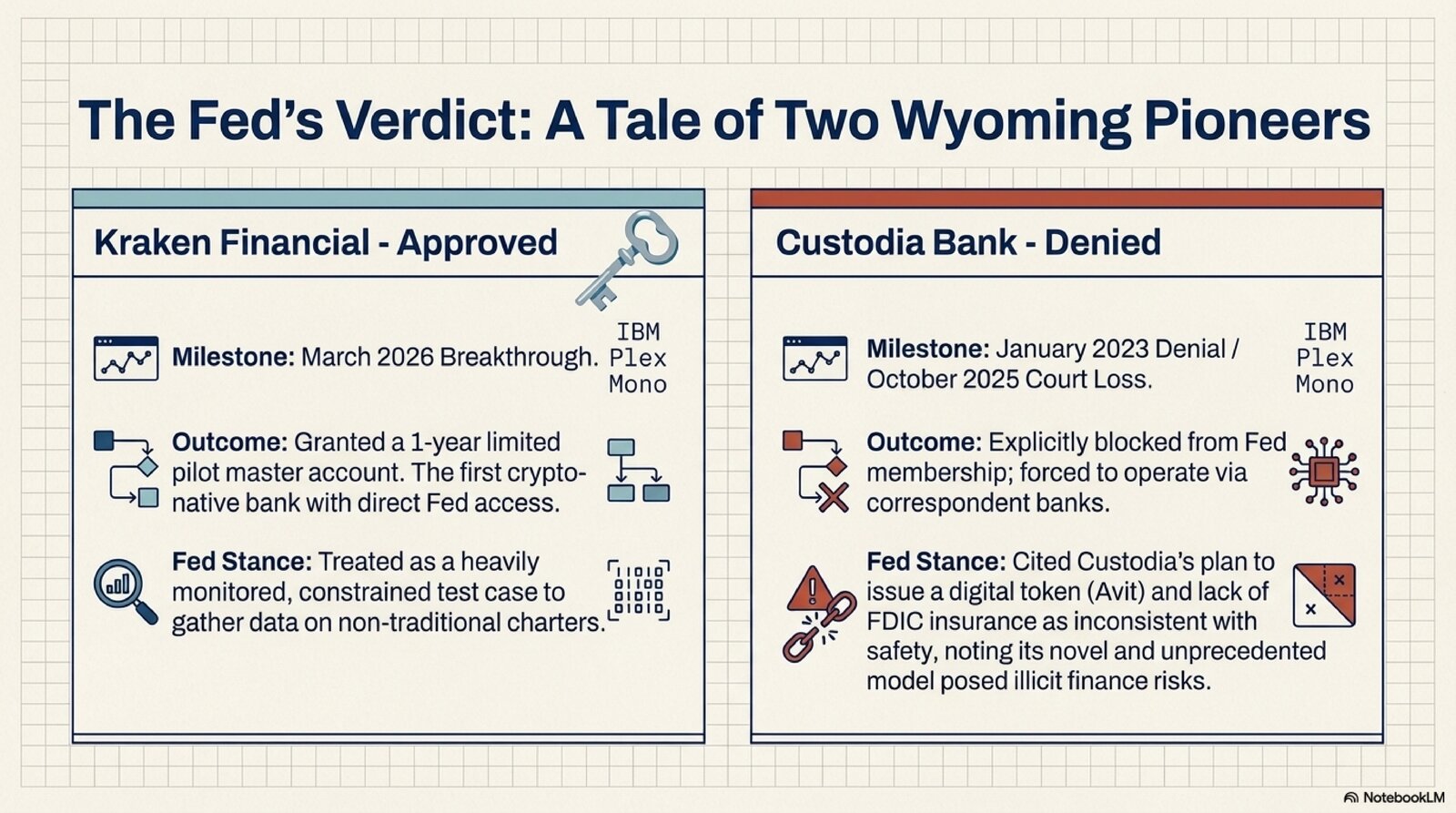

When Wyoming launched SPDIs, it implicitly expected them to get Fed accounts. SPDI deposits were meant to be kept at Fed or in cash/Treasuries, and an SPDI’s business model often requires an efficient way to move dollars. However, the Fed did not immediately welcome SPDIs:

- Custodia’s Denial: Custodia (formerly Avanti) applied to the Kansas City Fed for a master account in 2020 and waited over 18 months without a decision, eventually suing the Fed for delays. In early 2023, the Fed formally denied Custodia’s Federal Reserve membership application and, by extension, its master account request.[6] The Fed’s order (Jan 2023) was scathing: it cited Custodia’s business plan to focus heavily on crypto, its lack of federal deposit insurance, and gaps in its risk management as reasons for denying membership. The Fed concluded that Custodia’s acceptance would be “inconsistent with” required factors – essentially saying the risks were too high and too novel.

- Legal Battle: Custodia sued to compel a decision, then to overturn the denial. In October 2025, the U.S. 10th Circuit Court of Appeals ruled against Custodia, affirming that the Fed has discretion to protect the payment system.[13] The court’s majority deferred to the Fed’s judgment on risk; a dissenting judge famously remarked that denying a master account to a bank effectively is “akin to a death sentence” for that bank’s business model. Nevertheless, Custodia’s fight ended with that loss, leaving it operational but without direct Fed access.

- Fed’s New Guidelines: The high-profile nature of these applications prompted the Federal Reserve to issue guidelines in mid-2022 for evaluating such requests.[7] The Fed established a tiered review system:

- Tier 1: Federally insured banks (easiest path).

- Tier 2: Uninsured institutions subject to federal supervision (like OCC-chartered trust banks).

- Tier 3: Uninsured institutions not federally supervised – the bucket that includes SPDIs and potentially DADIs. Tier 3 applicants face the toughest scrutiny.

- Cracking the Door Open – Kraken’s Approval: In a surprising and significant move, the Federal Reserve Bank of Kansas City approved a master account for Kraken’s SPDI (Payward/Kraken Financial) in March 2026.[8] However, this wasn’t a full embrace. It’s described as a “limited purpose” account for an initial one-year term. Essentially, it’s a pilot program. Kraken can now hold funds at the Fed and directly clear payments, but presumably under close oversight and limits. Fed Vice Chair for Supervision, Michelle Bowman, called Kraken’s account a “pilot program” to gather data on non-traditional banks accessing the Fed.

“With a Federal Reserve master account, we can operate not as a peripheral participant... but as a directly connected financial institution.” — Kraken co-CEO[14]

Kraken’s achievement made it the first crypto firm with direct Fed access – a milestone five years in the making.

Nebraska DADI and the Fed

Nebraska anticipated the Fed issue from the start. NFIA explicitly authorizes a digital asset depository “to make an application to become a member bank of the Federal Reserve System.” That wording is notably direct. It signals Nebraska’s intent that their institutions become Fed members (which implies getting access to the Fed’s accounts and services).

As of early 2026, no Nebraska DADI has yet applied for a Fed account (Telcoin’s charter was finalized only in late 2025). Telcoin is expected to pursue Federal Reserve membership when appropriate, likely using the success of Kraken as part of its case. Telcoin’s model might even appeal to the Fed more: by holding its reserves in FDIC-insured banks, Telcoin’s risk profile could be seen as somewhat more traditional. Moreover, if Telcoin’s stablecoin is transacting mostly in the consumer remittance space, volumes might be more predictable and less interwoven with volatile crypto trading, potentially making the Fed a bit more comfortable.

The “Skinny Account” Concept

The Fed and commentators have floated the idea of offering limited Fed accounts to novel charters – essentially giving them access to payment rails and interest on reserves, but perhaps ring-fencing usage. For example, a “skinny” account might forbid overdrafts (which is fine for full-reserve banks) and might limit services to just storing funds and transferring out to designated counterparties, without access to Fed credit facilities. Bowman’s comments in March 2026 indicate Kraken’s master account is being treated as a sort of pilot as they iron out what conditions to impose broadly. If it goes well (no incidents, smooth operations, effective compliance), that bodes well for others like Telcoin or even Custodia (which conceivably could reapply down the road).

Implications of Fed Access

- For the banks: having a master account dramatically improves their service offerings and credibility. It means they can clear payments 24/7 (via FedNow, the new instant payment service, or traditional networks) and hold customer fiat as a digital balance at the Fed – the safest asset possible. It also means earning interest on reserves (the Fed pays interest on reserve balances; at times that’s a substantial revenue source).

- For the crypto ecosystem: a crypto bank with a Fed account can bridge decentralized finance and central bank money. For example, a user could swap a token for eUSD and know that eUSD is directly redeemable for Fed-held dollars. It brings a level of trust and finality that wasn’t there with stablecoins backed by offshore or opaque treasuries.

- For the Fed and regulators: letting these entities in means they need to be supervised equivalently to other banks. There’s also a policy angle: If state banks provide stablecoins, that could either complement or complicate any U.S. central bank digital currency (CBDC) plans.

In summary, while the state laws opened the gate to the Fed, the Federal Reserve itself has been the cautious gatekeeper, only now starting to inch it open. Nebraska’s charter is poised to test those waters in the near future, and Wyoming’s persistence has begun paying off with Kraken. The interplay between innovative state laws and conservative federal oversight will likely continue to evolve.

9. Case Studies of First Chartered Institutions

To put all these legal and operational details into context, let’s examine the real-world entities that have emerged under Wyoming’s SPDI and Nebraska’s DADI charters. These early adopters illustrate how each framework is being used – their business models, progress, and challenges.

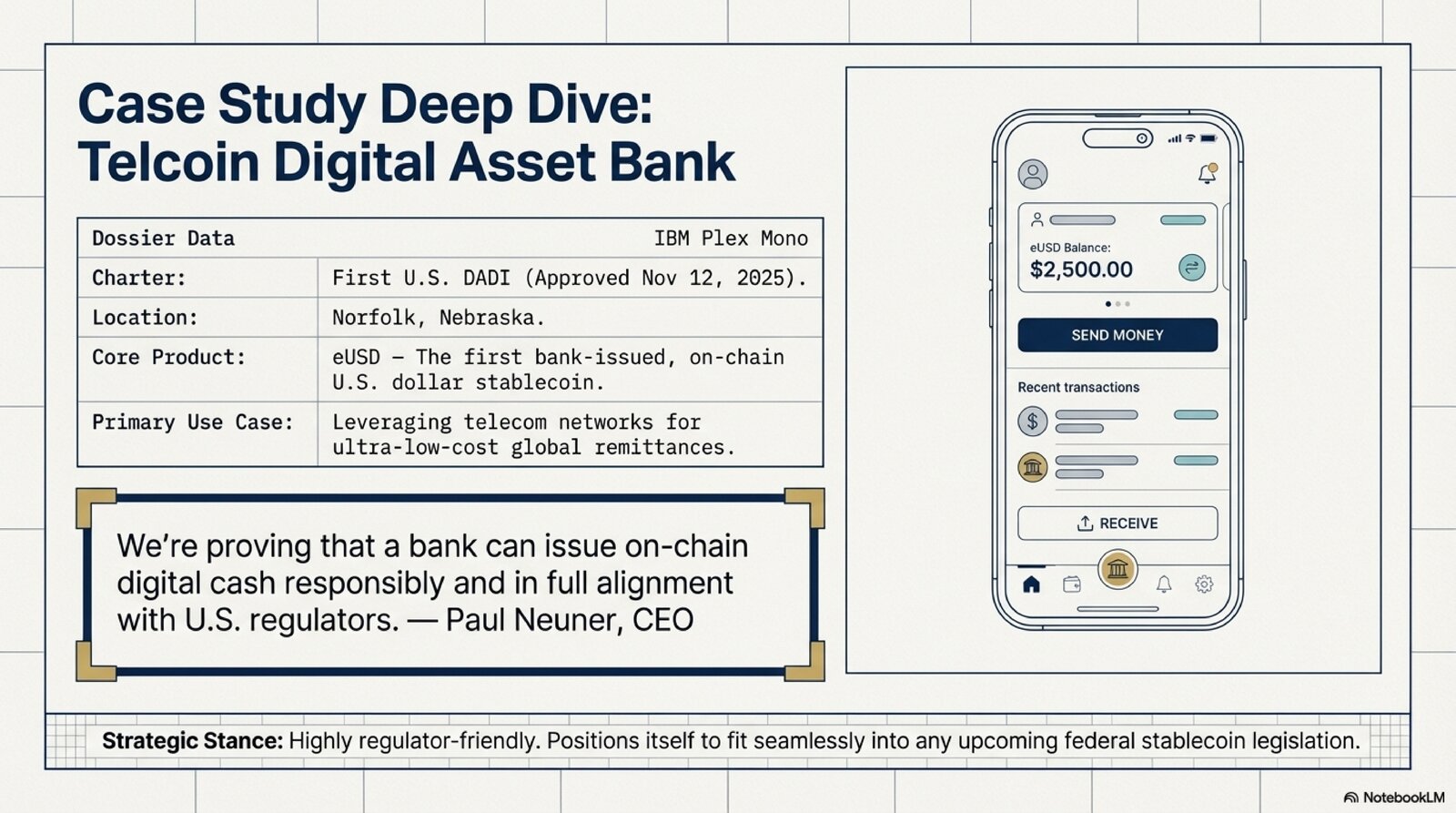

Telcoin Digital Asset Bank (Nebraska)

- Charter Approved: November 12, 2025[15] – the first (and as of 2026, only) DADI charter.

- Location: Headquarters in Norfolk, Nebraska (with a presence in Lincoln for regulatory liaison).

- Business Focus: Telcoin is fundamentally a fintech/telecom crossover. The parent company, Telcoin, Inc., launched in 2017 with the concept of leveraging telecom networks (mobile phones) to provide affordable remittances and digital financial services via blockchain. The Telcoin Digital Asset Bank is pivotal to this plan: it will issue eUSD stablecoins – effectively digital cash – and integrate them into a mobile app that lets users convert between eUSD and local currency, send payments abroad, earn yield, etc.

- Stablecoin (eUSD): eUSD is a U.S. dollar stablecoin issued by Telcoin’s bank and advertised as “the first bank-issued, on-chain U.S. dollar stablecoin.”[16] Each eUSD token is fully backed by actual USD deposits or short-term Treasuries. Telcoin’s press release highlighted that unlike “unregulated, offshore” stablecoins, eUSD comes with the trust of a regulated bank. They believe this trust factor will drive adoption, especially among telecom partners and their customers who might not otherwise touch crypto.

- Services: Beyond stablecoin issuance, Telcoin Bank will provide digital asset custody, fiat on/off ramps connecting bank accounts to blockchain, compliant yield on stablecoin deposits, and partnering with local community banks nationwide to help them get into blockchain.

- Regulatory Posture: Telcoin’s messaging has been very regulator-friendly. CEO Paul Neuner stated, “We’re proving that a bank can issue on-chain digital cash responsibly and in full alignment with U.S. regulators.” They consciously set themselves apart from more combative crypto firms.

- Outlook: Telcoin now must execute on deploying eUSD at scale. They’ve indicated remittance corridors as a key use: imagine a worker in the U.S. converting dollars to eUSD via Telcoin, sending eUSD to a family member abroad, who then cashes out via a local telecom partner. Fees could be cents rather than traditional remittance fees of 5–7%. If they succeed, it validates Nebraska’s approach and could lead to more DADI applications.

Kraken Financial (Wyoming)

- Charter Approved: September 16, 2020[17] – the first SPDI charter ever.

- Location: Cheyenne, Wyoming.

- Parent Company: Kraken is one of the world’s largest cryptocurrency exchanges. By volume, it’s often in the global top 5 and serves millions of users.

- Business Focus: Kraken’s rationale for the SPDI was to create an in-house bank to serve its exchange and clients. With the SPDI, Kraken can onboard U.S. customers directly, handle internal dollar movements without external wires, custody user crypto wallets in a regulated entity, and issue debit cards for seamless real-world spending.

- Services: Digital asset debit cards, wealth management and staking services, seamless online banking experience, and potentially IRA accounts for crypto. With the Fed account, a new service could be corporate treasury management.

- Current Status: After the March 2026 master account approval, Kraken Financial announced it would gradually roll out services, prioritizing large traders and institutions who benefit from faster fiat on/off ramps. It’s a cautious go-live under the Fed’s eye.

- Significance: Kraken Financial’s journey is precedent-setting. It will show whether a crypto exchange can actually incorporate as a bank and meet all the regulatory expectations. If yes, it may encourage others (Coinbase, Gemini, etc., may take note).

Custodia Bank (Wyoming)

- Charter Approved: October 2020 (as Avanti Bank & Trust).[12]

- Location: Cheyenne, Wyoming.

- Founder: Caitlin Long, a former Wall Street banker turned blockchain advocate who was instrumental in Wyoming’s crypto legislation.

- Business Focus: Custodia’s vision was to blend crypto services with the traditional financial system for institutional clients. It planned to offer custody of crypto assets for institutions, a real-time payment system for B2B transactions using a digital asset (Avit) that could settle nearly instantly 24/7, and banking services to crypto companies who were underserved by traditional banks.

- The Avit Token: This was essentially a stablecoin by another name, but structured legally as a special type of instrument. It was supposed to be issued in exchange for dollars and fully reserved.

- Setback at the Fed: Custodia’s ambitious plan hit a wall at the Federal Reserve. Its membership was denied, and subsequent legal actions failed.[6][13] The Fed’s rejection effectively prevents Custodia from offering the full suite of services it envisioned.

- Current Status: Custodia remains a Wyoming-chartered bank but, lacking Fed access, it pivoted to more of a custodial and consulting model. It has also become somewhat of a policy advocate, pushing for fair access to Fed services.

- Outlook: If Kraken’s pilot goes well, Custodia could reapply or adjust its model to address the Fed’s concerns.

Wyoming Deposit & Transfer (WDT)

- Charter Approved: June 2021 – Wyoming’s third SPDI.

- Focus: WDT came from a group of former financial services professionals. Its angle is to be a “bankers’ bank” for digital assets – providing behind-the-scenes services to fiduciaries (trust companies, broker-dealers) and blockchain firms.

- Status: WDT hasn’t been very public. They presumably have built the technology and awaited regulatory green lights. Their CEO, Julie Fellows, emphasized working closely with regulators and meeting institutions’ needs in a compliant way.

Commercium Financial

- Charter Approved: August 2021 – the fourth SPDI.

- Vision: Commercium branded itself as “the first US digital bank to tokenize real world assets.” It intended to handle things like tokenized securities or real estate – bridging traditional assets onto blockchain.

- Significance: Commercium shows how Wyoming’s SPDI concept was broad – it wasn’t just for handling cryptocurrency, but any digital asset including tokenized traditional assets.

To summarize the cast:

- Nebraska has Telcoin Digital Asset Bank – a fintech-driven stablecoin and remittance bank.

- Wyoming has Kraken – an exchange-driven crypto bank; Custodia – an entrepreneur-driven bank focusing on institutional and payments innovation; WDT – a service provider bank for fintechs/fiduciaries; and Commercium – a tokenization-focused bank.

- As of 2026, Telcoin and Kraken are the ones making tangible strides (Telcoin just launched, Kraken just got Fed access). Custodia is in a holding pattern, and the others are likely awaiting market or regulatory signals.

The experiences of these institutions will heavily influence how attractive and effective the SPDI/DADI charters appear going forward.

10. Side-by-Side Comparison of Key Features

To highlight the similarities and differences between Wyoming’s SPDI charter and Nebraska’s DADI charter, the following table outlines their key attributes:

| Aspect | Wyoming SPDI | Nebraska DADI |

|---|---|---|

| Enabling Law & Date | Enacted by HB 74 in Feb 2019, creating SPDI Act (W.S. 13-12-101 et seq.). Effective October 2019. Wyoming also updated related laws (UCC via SF125 in 2019) for digital assets. Amendments: 2020 (clarifications) and 2021 (digital asset custody rules) to refine the framework. | Enacted by LB 649 in May 2021 as the Nebraska Financial Innovation Act, codified at Neb. Rev. Stat. §§ 8-3001 to 8-3031. Effective October 1, 2021. Amendments: 2023 (via LB 92) updated certain provisions (e.g. clarifying definitions, director’s powers). |

| Charter Purpose | Create full-reserve banks that can handle digital assets and provide limited banking services (deposit-taking, custody, fiduciary activities) but no lending. Intended to serve blockchain and fintech firms that need banking without engaging in credit or maturity transformation. | Create digital asset depository institutions – essentially crypto-friendly banks – either as stand-alone banks or departments of existing banks. They hold digital assets and provide payment and custody services, aiming to integrate fintech (like stablecoin issuers) into the regulated banking fold. No traditional lending or demand deposit activities. |

| Regulator | Wyoming Division of Banking (State Banking Commissioner and Banking Board). The Banking Board approves charters; Division conducts exams and issues rules. SPDIs follow Wyoming banking regs, with specific SPDI rules for capital, liquidity, custody, etc. No routine federal regulator (unless Fed membership obtained). | Nebraska Dept. of Banking and Finance (NDBF). NDBF Director approves charters and regulates DADIs under NFIA and general Nebraska banking laws. NDBF promulgates rules (with recent updates for clarity). Federal oversight only if the institution obtains Fed membership (none yet as of 2026). |

| Eligible Organizers | 5 or more individual incorporators (standard for state bank) or an existing Wyoming bank converting. Must include “SPDI” or similar in name to denote special status. | Either new incorporation by 5+ persons (including at least 1 Nebraska resident) to form a digital asset bank, or an existing Nebraska-chartered bank can apply to add a digital asset depository department via charter amendment. New institutions must have “digital asset bank” (or similar) in their name. |

| Initial Capital Requirement | Statutory minimum $5 million[10] capital stock to charter. Also must demonstrate funds for operating expenses (initially 3 years, amended to 1 year by 2021)[11] and set up a contingency fund (2% of assets) – latter was later repealed in 2021. Regulatory practice: The Banking Commissioner has required much higher capital based on business model. Guidance suggested $10–30 million likely needed in many cases. | Minimum $10 million[2] in capital stock must be fully subscribed before filing an application (funds held in escrow until charter approved). Must also provide a surplus sufficient for ~3 years of operating expenses (or amount set by NDBF). Bank holding companies may invest in DADIs (up to 10% of their capital, or more with approval). |

| Deposit Abilities | Can accept deposits in any currency (fiat or crypto), but no demand deposit accounts for retail withdrawal by check. Typically focuses on business and institutional deposits or operational accounts. | Can accept “digital asset deposits” (cryptocurrency held in custody or on deposit). May accept U.S. currency from customers only for safekeeping or facilitating digital asset transactions, not for third-party payments. Prohibited from offering any deposit account that functions like a checking account. |

| Lending Abilities | No lending of any kind with customer deposits. SPDIs cannot extend credit, issue loans, or otherwise deploy depositor funds in loans. They can, however, conduct other permissible bank investments and engage in repurchase agreements within regulatory limits. | No fiat lending allowed. Explicitly banned from consumer loans, commercial loans, mortgages, or even overdraft credit lines. They may facilitate digital asset lending/borrowing services (e.g., connecting customers to DeFi or providing custody for a borrower-lender arrangement) as long as the bank’s own assets aren’t at risk. |

| Reserve Requirements | Must maintain unencumbered liquid assets ≥ 100% of deposit liabilities at all times. Liquid assets defined by statute include cash, balances at Fed or FDIC banks, and Level 1 high-quality securities (e.g., Treasuries). State rules expand this to certain AA/AAA-rated corporate or municipal bonds. | Must maintain “liquid assets valued at not less than one hundred percent of its digital asset deposits.” Liquid assets include U.S. currency (on hand or on deposit in a Fed or FDIC-insured bank) and highly liquid investments like U.S. government securities. NFIA specifically requires that any USD received from a customer be held in an FDIC-insured Nebraska bank. |

| Stablecoin Issuance | Not explicitly addressed in statute. Permissible as an incidental activity, subject to regulator approval. Custodia’s proposed “Avit” token was a stablecoin-like product, but the Fed’s rejection cited concerns with this novel aspect. No Wyoming SPDI has launched its own stablecoin to date. | Expressly authorized. NFIA allows a digital asset depository to “issue stablecoins… and hold stablecoin reserves at an FDIC-insured financial institution.” The first DADI, Telcoin, is issuing eUSD, a USD-pegged stablecoin fully backed by USD and U.S. Treasuries held in Nebraska banks. Nebraska is the first state to have a bank officially “mint” stablecoins under regulation. |

| Digital Asset Custody | Core business for SPDIs. They can hold cryptocurrencies and other digital assets in custody as a fiduciary or bailee. Wyoming’s digital asset statutes and regulations set standards for custody (segregation of assets, cyber controls, private key management). SPDI rules allow these banks to serve as qualified custodians under SEC rules for investment advisers. | Likewise a central function. DADIs can custody crypto and act as qualified custodians for digital assets. NFIA and Nebraska’s UCC amendments accommodate treatment of digital assets as “controllable electronic records” for legal clarity. A DADI must keep customer digital assets segregated and follow any NDBF rules on custody safety. |

| Consumer Protection & Disclosures | High emphasis on transparency due to no FDIC insurance: SPDI customers must acknowledge in writing that their deposits are uninsured and that the bank operates under a different framework. Marketing materials must clearly state the special nature. | Extensive explicit requirements. NFIA §8-3008 lists at least 13 mandatory disclosures to customers, including: “Not FDIC insured; digital assets can be volatile and result in loss; the bank is new and innovative with associated risks; transactions may be irreversible; the customer is solely responsible for digital asset investment decisions,” etc. Nebraska also requires DADIs to maintain a public file on how they serve community needs. |

| FDIC Deposit Insurance | Not required and generally not available. By law, SPDIs are exempt from needing FDIC insurance because they don’t lend. No SPDI has FDIC insurance. The lack of insurance was one factor the Fed cited in treating SPDIs as riskier (Tier 3). | Not required/possible for digital asset accounts. NFIA institutions do not offer insured deposits to the public. Any USD funds from customers are actually held in traditional FDIC-insured banks, but once converted to a digital asset (or stablecoin) at the DADI, those are not insured claims. Customers get explicit notice of no FDIC coverage. |

| Federal Reserve Access | Eligible but not guaranteed. The Fed issued guidelines in 2022 treating SPDIs as Tier 3 (highest risk) applicants. In Jan 2023, the Fed denied Custodia’s application. In Mar 2026, the Kansas City Fed approved Kraken’s master account on a 1-year limited basis – the first SPDI (and first crypto firm) to gain Fed access. Conditions likely apply. | Explicitly authorized to seek Fed membership. No DADI has yet obtained a Fed master account (Telcoin is expected to apply in the near future). Nebraska structured its law hoping to ease Fed acceptance. A Nebraska DADI falls in the same Fed review Tier 3 as SPDIs (state-chartered, uninsured). As of early 2026, Fed access for DADIs is aspirational but not yet realized. |

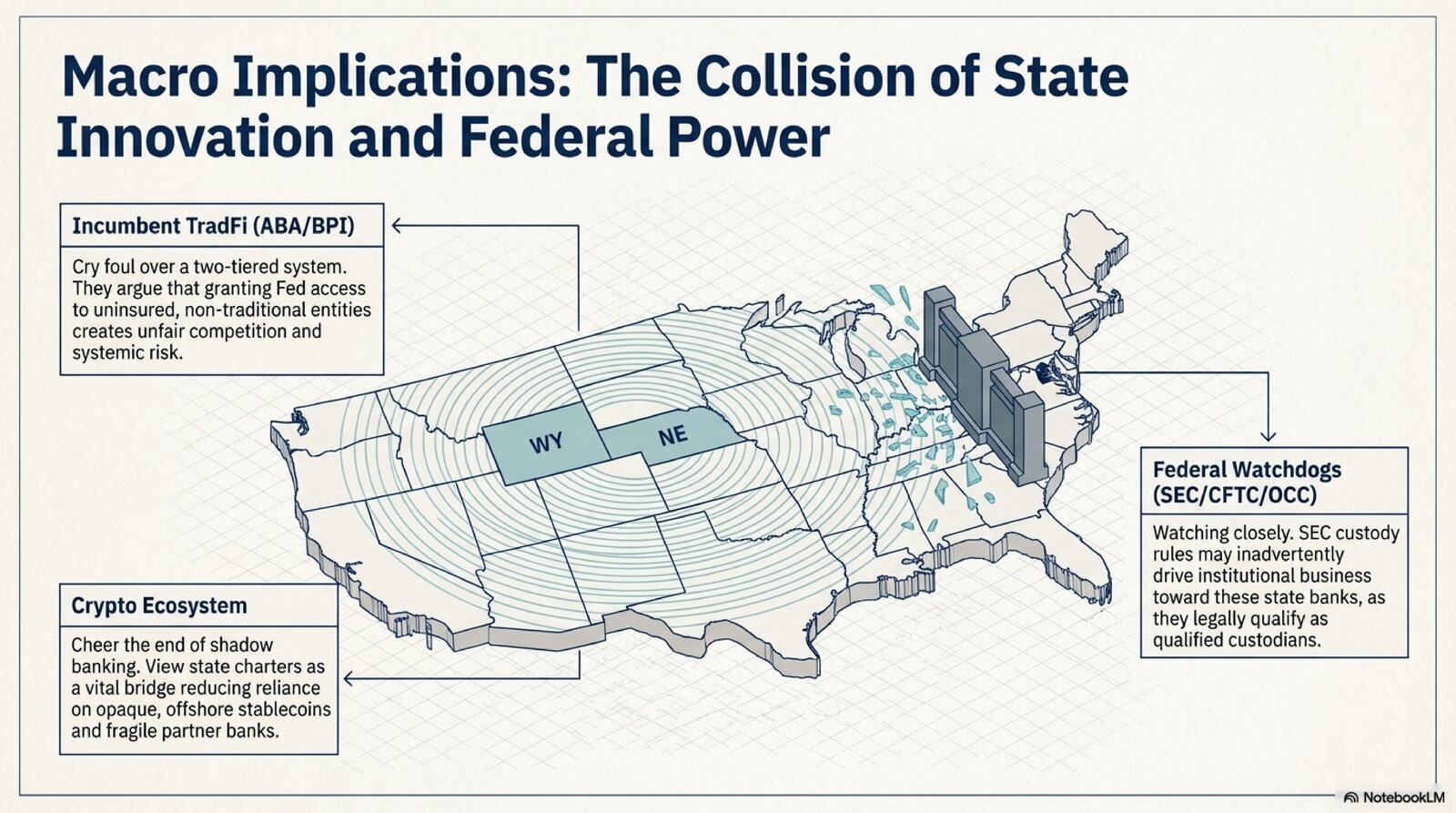

11. Policy Implications and Regulatory Reactions

The advent of Wyoming’s SPDI and Nebraska’s DADI charters has provoked significant discussion in financial regulatory circles. These state initiatives effectively challenged the traditional federal oversight paradigm, prompting responses at multiple levels of government and within the industry.

Federal Regulatory Stance

Federal banking regulators – the Fed, OCC, FDIC – have approached crypto banks cautiously, often skeptically:

- The Federal Reserve set up a three-tier system to assess novel charters’ access to accounts. This was a direct response to Wyoming’s chartering of SPDIs. By placing them in Tier 3, the Fed signaled heightened concern. In denying Custodia, the Fed Board underscored that an uninsured, crypto-focused bank concentrating in one sector posed “significant safety and soundness risks.” Even as Kraken’s limited account was approved, the Fed’s tone was measured: Kansas City Fed’s president emphasized the priority of “integrity and stability of the payments system.”

- The OCC (Office of the Comptroller of the Currency) took a different route during 2020–21 by granting a few national trust charters to crypto firms (Anchorage, Paxos, Protego). These are narrower than banks (trust charters can’t take deposits easily), but signaled a willingness to integrate crypto under federal charters. However, under subsequent leadership, the OCC has pulled back some – in 2023 it said it would pause new crypto charters.

- The FDIC has been openly concerned about crypto risks to banks. In 2022–2023, it instructed the banks it supervises to monitor crypto exposure and in some cases to reduce engagement. Notably, when two crypto-friendly traditional banks (Silvergate Bank and Signature Bank) failed in March 2023, regulators became even warier.

- The SEC and CFTC, while not bank regulators, have stakes here too. The SEC has proposed rules that would make it harder for investment advisers to use any custodian that isn’t a “qualified custodian” in the traditional sense, implicitly excluding many crypto firms. However, a state or federally chartered bank like SPDIs/DADIs are qualified custodians, which could give them a leg up in serving institutional investors.

In May 2025, the OCC issued Interpretive Letter 1184, further clarifying that national banks and federal savings associations may provide cryptocurrency custody services, buy and sell crypto assets held in custody at the customer’s direction, and outsource crypto custody to qualified third-party sub-custodians. Building on earlier OCC Interpretive Letters 1170 and 1183, IL 1184 solidified the position that federally chartered banks have clear authority to engage in crypto custody without needing prior supervisory non-objection. This established a parallel federal pathway: large, established financial institutions can now custody digital assets under their existing OCC charters without needing a state SPDI or DADI charter.

Congressional Interest

The innovation by Wyoming and Nebraska has not gone unnoticed by Congress:

- Senator Cynthia Lummis (R-WY) has been a vocal advocate. She co-authored the Lummis-Gillibrand Responsible Financial Innovation Act, a comprehensive crypto bill, which among many things, acknowledges new state charters. Lummis has often cited Wyoming’s SPDI as an example of how states can lead and has criticized the Fed’s slow-walking of applications.

- Stablecoin Legislation: The fact that Telcoin’s bank can issue a stablecoin touches on discussions in Congress about stablecoin regulation. In 2022–2023 drafts emerged that would require stablecoin issuers to be depository institutions (banks) or similar regulated entities. Nebraska preemptively created a pathway for exactly that. If Congress passes something like that in the future, Nebraska could become a magnet for stablecoin projects wanting a quick state charter to comply.

- Federal Fintech Charter vs. State Charters: A few years ago, the OCC floated a “fintech charter” (special purpose national bank charter for non-deposit-taking fintechs). That was litigated and never really implemented broadly. Wyoming’s and Nebraska’s moves somewhat filled that gap at the state level.

On July 18, 2025, President Trump signed the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) into law — the first federal regulatory framework for payment stablecoins. The Act requires stablecoin issuers to maintain one-to-one reserves and allows issuers with not more than $10 billion in outstanding stablecoins to opt for state-level regulation. This directly validates Nebraska’s approach: DADI-chartered banks issuing stablecoins under state supervision now operate within a recognized federal framework.

Industry Reactions

- Traditional Banks: Incumbent banks, especially smaller community banks, have had mixed feelings. Some see opportunity – e.g., a community bank in Nebraska could launch a digital asset department to diversify offerings. Many banks, via trade groups (ABA, BPI, ICBA), have been critical, arguing these new charters enjoy loopholes (no FDIC insurance, different capital rules) yet want Fed privileges, which they say could create unfair competition or systemic risk. The BPI’s October 2020 blog “Beware the Kraken” basically argued that SPDIs are a recipe for instability.

- Crypto Industry: Many crypto firms have cheered these frameworks as crucial breakthroughs. Having a regulated crypto bank can provide plumbing that the industry sorely needs. The failures of Silvergate and Signature (which were two of the few traditional banks serving crypto companies) left a void; SPDIs like Kraken are stepping in to fill it.

- State vs State: Other states have been watching. Illinois proposed a Special Purpose Trust Bank charter in 2021, but it didn’t pass. Texas in 2021 clarified state banks can custody crypto under existing law. Now that Nebraska and Wyoming have paved the way, if their banks start showing economic benefits, other states may follow.

Monetary Policy & Financial Stability Considerations

A subtle but important implication of banks like these is how they might behave in stress scenarios:

- Because they can’t lend, they also don’t create money supply via fractional lending. That could actually be seen as positive for stability (no credit bubbles from them). But if they attract a lot of deposits from traditional banks, that could marginally reduce credit availability in the system.

- The Fed’s concern about “Pass-Through Investment Entities” (PTIEs) expressed worry that if heaps of institutional money flocked to a narrow bank that just parks it all at the Fed to earn interest on excess reserves, it could turn into an arbitrage that complicates monetary policy. To forestall that, the Fed considered maybe paying such entities a lower interest rate.

- On stability: Because SPDIs/DADIs don’t loan out, the chance of them failing due to asset quality is low. The bigger risk is operational or fraud risk, like a hack draining assets or a massive AML violation leading to fines.

These state charters are effectively acting as laboratories of innovation in bank regulation (echoing the Brandeis idea of states as laboratories). They’re testing whether the traditional bank regulatory framework, adjusted in certain ways, can accommodate 21st-century fintech activities.

12. Strategic Positioning and State-Level Innovation Goals

Wyoming and Nebraska embarked on these chartering experiments with distinct motivations and strategic visions, even as both share the broader goal of encouraging fintech innovation.

Wyoming’s Strategy – “Crypto Frontier”

- Economic Diversification: Wyoming, traditionally reliant on energy and minerals, saw blockchain technology as a sector to diversify its economy. By 2018, state legislators (spurred by a blockchain task force including Caitlin Long) passed a flurry of laws to signal “Wyoming is open for crypto business.” The SPDI was the capstone of that push, intended to solve the pain point of crypto companies being debanked. “Come to Wyoming, and we’ll let you be your own bank,” was essentially the pitch.

- First-Mover Advantage: Wyoming basked in being first. It used that in marketing – for a while, it was the only place for a crypto firm to get a bank charter. That pioneering reputation was meant to snowball – drawing more companies, more innovation.

- Regulatory Innovation: Wyoming took pride in crafting new legal concepts (like recognizing direct ownership of crypto through custody and the idea of a new bank type). It showed states can innovate faster than federal agencies.

- Long-Term Goal: Wyoming likely hopes that over time, as these institutions prove safe, federal law or policy will adapt and perhaps formally integrate them.

Nebraska’s Strategy – “Fintech Hub with a Focus”

- Preventing Brain Drain & Fostering Innovation: Senator Mike Flood often spoke about keeping Nebraska’s tech talent in-state. Telcoin was a Nebraska-based startup that might have taken its operations elsewhere if not for a supportive environment.

- Stablecoin Leadership: Nebraska carved out a niche by explicitly embracing stablecoins. This was savvy timing: the stablecoin market was booming and on regulators’ radar. Being the first to have a state-regulated stablecoin bank gives Nebraska a voice in the national conversation. If stablecoins become mainstream in finance, Nebraska could become a specialized hub for stablecoin issuers (the way South Dakota became for credit card banks or Delaware for incorporation).

- Public-Private Collaboration: Nebraska’s approach involved close work between lawmakers, regulators, and the private sector. This coalition-building suggests Nebraska wants to integrate innovation with oversight rather than position itself as a rebel against federal norms.

- Midwest Fintech Appeal: Nebraska likely sees an opportunity to draw fintech companies that might not want to go to the coasts or Bermuda. With a central U.S. location and a hospitable regulatory environment, they could attract startups focusing on payments, agri-finance (imagine tokenized grain contracts?) or other digital asset ideas that benefit from being in the heartland.

Comparative Mindset

- Wyoming was more about “We’ll break ground and ask for forgiveness later if needed” – they knew some federal friction would come, but considered it worth the attempt to leap ahead.

- Nebraska’s stance was “We’ll innovate but keep one eye on D.C.” – they deliberately waited to see Wyoming’s initial progress (2019–2020) then crafted NFIA in 2021 with tweaks (like stablecoin rules) and baked-in the expectation of Fed membership to push that conversation.

- Both states tapped into a bit of states’ rights ethos: the idea that states can charter banks and shape financial services within their borders, an authority dating to 1863 (or even 1790s pre-National Bank Act days).

- Importantly, neither state wants these charters to fail catastrophically – that would tarnish their reputations. So Wyoming has been careful to only approve applicants that meet high standards (4 charters in 3+ years). Nebraska similarly took over a year to evaluate Telcoin’s application thoroughly (from Oct 2023 application to Nov 2025 final charter). This cautious approach indicates the states are prioritizing long-term credibility over quick growth.

Collaboration or Competition?

Initially, Wyoming had the field alone. Nebraska’s entry could be seen as competition, but also validation of the concept. There might be a healthy competition to attract businesses – e.g., will a firm like Circle (issuer of USDC stablecoin) consider a Nebraska charter because of stablecoin clarity? Or will they consider Wyoming? If Telcoin thrives, Wyoming might consider adding explicit stablecoin language to their laws to attract similar business (states often mimic each other’s successful laws).

At the end of the day, Wyoming and Nebraska both aim to embed themselves in the evolving digital economy by being friendly but responsible regulators. Their approaches reflect local values – Wyoming’s independent, pioneering spirit and Nebraska’s diligent, community-conscious ethos – applied to the new frontier of crypto banking.

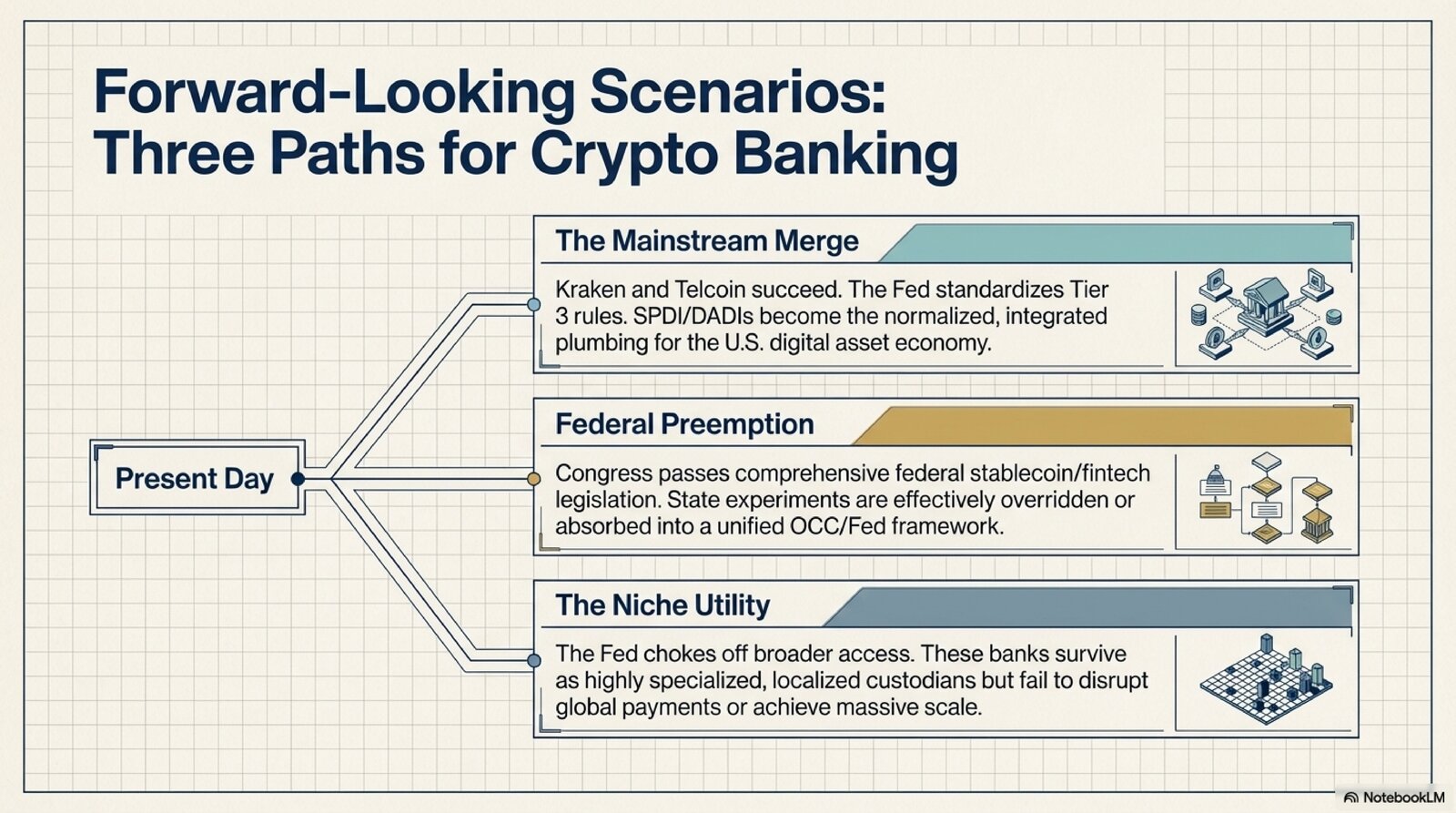

13. Forward-Looking Analysis: Implications for U.S. Crypto Banking Policy

As we look to the future, the experiences of Wyoming’s SPDI and Nebraska’s DADI charters will likely shape the trajectory of crypto banking in the United States in several key ways:

1. Proof of Concept and Scaling

First and foremost, these charters are still experimental. Over the next few years, their viability needs to be proven on metrics like:

- Safety and Soundness: Can these banks operate without major incidents (such as hacks, insolvencies, or compliance failures)? Regulators will watch like hawks. A clean track record will build confidence and could lead to more approvals (and maybe more charters). A mishap at one of these institutions, however, could set things back considerably by reinforcing fears that crypto-related banks are too risky.

- Market Demand: Do crypto firms and users actually utilize these banks at scale? If Kraken’s banking services lead to a surge in U.S. trading volume or new customers because they trust a regulated bank, that’s a positive sign. If Telcoin’s stablecoin gains user adoption beyond niche use, it shows a state-regulated token can compete with private stablecoins.

- Profitability & Sustainability: As business entities, these banks need sound economics. Full-reserve banks historically struggle with profitability because they can’t leverage deposits. They’ll need to find revenue in fees or ancillary services. Fortunately, the parent companies (Kraken, Telcoin) seem committed to supporting them as strategic arms, not necessarily big profit centers initially.

2. Influence on Federal Policy

- Regulatory Integration: If Wyoming and Nebraska banks succeed, federal regulators might integrate them into the mainstream by providing clearer pathways. For instance, the Fed might formalize that Tier 3 entities can get accounts with conditions (essentially codifying the Kraken pilot results for others).

- Legislative Action: On Capitol Hill, tangible examples are powerful. Lawmakers will use Kraken and Telcoin as case studies. If they’re positive, they strengthen arguments that appropriate regulation (not prohibition) of crypto activities works.

- Federal Chartering Options: Success at the state level might spur federal agencies to “jump in.” The OCC could resurrect a form of special charter focusing on payments or crypto custody, to allow a direct federal route.

3. Competitive Dynamics in Crypto Banking

The presence of regulated crypto banks will likely raise the bar for unregulated competitors:

- Stablecoins: Tether and Circle dominate stablecoins. If Telcoin’s bank shows that a fully regulated stablecoin can operate and perhaps even get direct Fed access, then the pressure mounts on others to either get similar regulation or face users/governments favoring the regulated option.

- Crypto Exchanges and Custodians: If Kraken’s integration of banking is a competitive advantage (faster settlements, more trust, less dependency on outside banks), other exchanges might follow. Some could pursue Wyoming charters or push for federal alternatives.